/archive-images.prod.global.a201836.reutersmedia.net/2011/09/16/2011-09-16T195013Z_03_GM1E79H07UH01_RTRRPP_0_GREECE.JPG)

“A policeman tries to extinguish a fire on a man after he set himself ablaze outside a bank branch in Thessaloniki in northern Greece September 16, 2011. The 55-year old man had entered the bank and asked for a renegotiation of his overdue loan payments on his home and business, according to police, which he could not pay, but was refused by the bank.”

AUSTERITY KILLS

http://guardian.co.uk/society/2013/may/15/recessions-hurt-but-austerity-kills

by Jon Henley / 15 May 2013

“The austerity programmes administered by western governments in the wake of the 2008 global financial crisis were, of course, intended as a remedy, a tough but necessary course of treatment to relieve the symptoms of debts and deficits and to cure recession. But if, David Stuckler says, austerity had been run like a clinical trial, “It would have been discontinued. The evidence of its deadly side-effects – of the profound effects of economic choices on health – is overwhelming.” Stuckler speaks softly, in the measured tones and carefully weighed terms of the academic, which is what he is: a leading expert on the economics of health, masters in public health degree from Yale, PhD from Cambridge, senior research leader at Oxford, 100-odd peer-reviewed papers to his name. But his message – especially here, as even the IMF starts to question chancellor George Osborne’s enthusiasm for ever-deeper budget cuts – is explosive, backed by a decade of research, and based on reams of publicly available data: “Recessions,” Stuckler says bluntly, “can hurt. But austerity kills.”

In a powerful new book, The Body Economic, Stuckler and his colleague Sanjay Basu, an assistant professor of medicine and epidemiologist at Stanford University, show that austerity is now having a “devastating effect” on public health in Europe and North America. The mass of data they have mined reveals that more than 10,000 additional suicides and up to a million extra cases of depression have been recorded across the two continents since governments started introducing austerity programmes in the aftermath of the crisis. In the United States, more than five million Americans have lost access to healthcare since the recession began, essentially because when they lost their jobs, they also lost their health insurance. And in the UK, the authors say, 10,000 families have been pushed into homelessness following housing benefit cuts. The most extreme case, says Stuckler, reeling off numbers he knows now by heart, is Greece. “There, austerity to meet targets set by the troika is leading to a public-health disaster,” he says. “Greece has cut its health system by more than 40%. As the health minister said: ‘These aren’t cuts with a scalpel, they’re cuts with a butcher’s knife.'” Worse, those cuts have been decided “not by doctors and healthcare professionals, but by economists and financial managers. The plan was simply to get health spending down to 6% of GDP. Where did that number come from? It’s less than the UK, less than Germany, way less than the US.”

The consequences have been dramatic. Cuts in HIV-prevention budgets have coincided with a 200% increase in the virus in Greece, driven by a sharp rise in intravenous drug use against the background of a youth unemployment rate now running at more than 50% and a spike in homelessness of around a quarter. The World Health Organisation, Stuckler says, recommends a supply of 200 clean needles a year for each intravenous drug user; groups that work with users in Athens estimate the current number available is about three. In terms of “economic” suicides, “Greece has gone from one extreme to the other. It used to have one of Europe’s lowest suicide rates; it has seen a more than 60% rise.” In general, each suicide corresponds to around 10 suicide attempts and – it varies from country to country – between 100 and 1,000 new cases of depression. In Greece, says Stuckler, “that’s reflected in surveys that show a doubling in cases of depression; in psychiatry services saying they’re overwhelmed; in charity helplines reporting huge increases in calls”. The country’s healthcare system itself has also “signally failed to manage or cope with the threats it’s facing”, Stuckler notes. “There have been heavy cuts to many hospital sectors. Places lack surgical gloves, the most basic equipment. More than 200 medicines have been destocked by pharmacies who can’t pay for them. When you cut with the butcher’s knife, you cut both fat and lean. Ultimately, it’s the patient who loses out.” Such phenomena, he says, “are just a few of many effects we’re seeing. And with all this accumulation of across-the-board, eye-watering statistics, there’s a cause-and-effect relationship with austerity measures. These issues became apparent not when the recession hit Greece, but with austerity.” But public health disasters such as Greece’s are not inevitable, even in the very worst economic downturns. Stuckler and Basu began to look at this before the crisis hit, studying how large personal economic shocks – unemployment, loss of your home, unpayable debt – “literally could get under people’s skin, and cause serious health problems”.

The pair examined data from major economic upsets in the past: the Great Depression in the US; post-communist Russia’s brutal transition to a market economy; Sweden’s banking crisis in the early 1990s; the East-Asian debacle later that decade; Germany’s painful labour market reforms early this century. “We were looking,” Stuckler says, “at how rises in unemployment, which is one indicator of recession, affected people’s health. We found that suicides tended to rise. We wanted to see if there was a way these suicides could be prevented.” It rapidly became clear “there was enormous variation across countries”, he says. “In some countries, politicians managed the consequences of recession well, preventing rising suicides and depression. In others, there was a very close relationship between ups and downs in the economy and peaks and valleys in suicides.” Investment in intensive programmes to help people return to work – so-called Active Labour Market Programmes, well developed in Sweden (where suicides actually fell during the banking crisis) but also effective in Germany – were a factor that seemed to make a big difference. Maintaining spending on broader social protection and welfare programmes helped, too: analysis of data from the 1930s Great Depression in the US showed that every extra $100 per capita of relief in states that adopted the American New Deal led to about 20 fewer deaths per 1,000 births, four fewer suicides per 100,000 people and 18 fewer pneumonia deaths per 100,000 people. “When this recession started, we began to see history repeat itself,” says Stuckler. “In Spain, for example, where there was little investment in labour programmes, we saw a spike in suicides. In Finland, Iceland, countries that took steps to protect their people in hard times, there was no noticeable impact on suicide rates or other health problems. “So I think we really noticed these harms aren’t inevitable back in 2008 or 2009, early in the recession. We realised that what ultimately happens in recessions depends, essentially, on how politicians respond to them.” Poorer public health, in other words, is not an inevitable consequence of economic downturns, it amounts to a political choice – by the government of the country concerned or, in the case of the southern part of the eurozone, by the EU, European Central Bank and IMF troika.

Stuckler seizes on Iceland as an example of “an alternative. It suffered the worst banking crisis in history; all three of its biggest banks failed, its total debt jumped to 800% of GDP – far worse than what any European country faces today, relative to the size of its economy. And under pressure from public protests, its president put how to deal with the crisis to a vote. Some 93% of the population voted against paying for the bankers’ recklessness with large cuts to their health and social-protection systems.” And what happened? Under Iceland’s universal healthcare system, “no one lost access to care. In fact more money went into the system. We saw no rise in suicides or depressive disorders – and we looked very hard. People consumed more locally sourced fish, so diets have improved. And by 2011, Iceland, which was previously ranked the happiest society in the world, was top of that list again.” What also bugs Stuckler – an economist as well as a public-health expert – is that neither Iceland nor any other country that “protected its people when they needed it most” did so at the cost of economic recovery. “It didn’t break them to invest in programmes to help people get back to work,” he says, “or to save people from homelessness. Iceland now is booming; unemployment fell back to below 5% and GDP growth is above 4% – far exceeding any of other European countries that suffered major recessions.” Countries such as those in Scandinavia that took what Stuckler terms “wise, cost-effective and affordable steps that can make a difference” have seen the impact reflected not just in improved health statistics, but also in their economies. Which is why, occasionally, the austerity argument angers him. “If there actually was a fundamental trade-off between the health of the economy and public health, maybe there would be a real debate to be had,” he says. “But there isn’t. Investing in programmes that protect the nation’s health is not only the right thing to do, it can help spur economic recovery. We show that. The data shows that.” Drilling into the data shows the fiscal multiplier – the economic bang, if you like, per government buck spent, or cost per buck cut – for spending on healthcare, education and social protection is many times greater than that for money ploughed into, for example, bank bailouts or defence spending. “That,” says Stuckler, “seems to me essential knowledge if you want to minimise the economic damage, to understand which cuts will be the least harmful to the economy. But if you look at the pattern of the cuts that have happened, it’s been the exact opposite.” So in this current economic crisis, there are countries – Iceland, Sweden, Finland – that are showing positive health trends, and there are countries that are not: Greece, Spain, now maybe Italy. Teetering between the two extremes, Stuckler reckons, is Britain. The UK, he says, is “one of the clearest expressions of how austerity kills”. Suicides were falling in this country before the recession, he notes. Then, coinciding with a surge in unemployment, they spiked in 2008 and 2009. As unemployment dipped again in 2009 and 2010, so too did suicides. But since the election and the coalition government’s introduction of austerity measures – and particularly cuts in public sector jobs across the country – suicides are back.

Ministers seem unwilling to address the increase in suicides, arguing it is too early to conclude anything from the data. Stuckler points out that this is because the Department of Health prefers to use three-year rolling averages that even out annual fluctuations. But based on the actual data, he is in no doubt. “We’ve seen a second wave – of austerity suicides,” he says. “And they’ve been concentrated in the north and north-east, places like Yorkshire and Humber, with large rises in unemployment. Whereas London … We’re now seeing polarisation across the UK in mental-health issues.” He cites, also, the dire impact on homelessness – falling in Britain until 2010 – of government cuts to social housing budgets, and the human tragedies triggered by the fitness-for-work evaluations, designed to weed out disability benefit fraud. “What’s so particularly tragic about those,” he says, “is that the government’s own estimates of fraud by persons with disabilities is less than the sum of the contract awarded to the company carrying out the tests.” At least, though, no one in the UK has been denied access to healthcare – yet. Stuckler confesses to being “heartbroken” as what he sees happening to the NHS. “Britain stood out as the great protector of its people’s health in this recession,” he says. “By all measures – public satisfaction, quality, access – the UK was at or near the top, and at very low relative cost.” But that, he says, is now changing. “I don’t know if people quite realise how fundamental this government’s transformation of the NHS is,” he says. “And once it’s in place, it will be difficult, if not impossible, to reverse. We haven’t yet seen here what can happen when people are denied access to healthcare, but the US system gives us a pretty clear warning.” He finds this all in stark and depressing contrast to the post-second world war period, when Britain’s debt was more than 200% of GDP (far higher than any European country’s today, bar Iceland) and the country’s leaders responded not by cutting spending but by founding the welfare state – “paving the way, incidentally, for decades of prosperity. And within 10 years, debt had halved.”

The Body Economic should come as a broadside, morally armour-plated and data-reinforced. The austerity debate, Stuckler says, is “a public discussion that needs to be held. Politicians talk endlessly about debts and deficits, but without regard to the human cost of their decisions.” What its authors hope is that politicians will take the message they have uncovered in the data seriously, and start basing policy on evidence rather than ideology. (Some already do. When Stuckler and Basu presented some of their findings in the Swedish parliament, the MPs’ response was: “Why are you telling us this? We know it. It’s why we set up these programmes.” Others, notably in Greece, have sought to divert responsibility.) “Our book,” says Stuckler, “shows that the cost of austerity can be calculated in human lives. It articulates how austerity kills. It shows austerity and health is always a false economy – no matter how positively some people view it, because for them it shrinks the role of the state, or reduces payments into a system they never use anyway.” When times are hard, governments need to invest more – or, at the very least, cut where it does least harm. It is dangerous and economically damaging to cut vital supports at a time when people need them most. “So there is an opportunity here,” Stuckler concludes, “to make a lasting difference. To set our economies on track for a happier, healthier future, as we did in the postwar period. To get our priorities as a society right. It’s not yet too late. Almost, but not quite.”

‘NATURAL EXPERIMENT’

http://nytimes.com/2013/05/13/opinion/how-austerity-kills.html

by David Stuckler & Sanjay Basu / May 12, 2013

“Early last month, a triple suicide was reported in the seaside town of Civitanova Marche, Italy. A married couple, Anna Maria Sopranzi, 68, and Romeo Dionisi, 62, had been struggling to live on her monthly pension of around 500 euros (about $650), and had fallen behind on rent. Because the Italian government’s austerity budget had raised the retirement age, Mr. Dionisi, a former construction worker, became one of Italy’s esodati (exiled ones) — older workers plunged into poverty without a safety net. On April 5, he and his wife left a note on a neighbor’s car asking for forgiveness, then hanged themselves in a storage closet at home. When Ms. Sopranzi’s brother, Giuseppe Sopranzi, 73, heard the news, he drowned himself in the Adriatic. The correlation between unemployment and suicide has been observed since the 19th century. People looking for work are about twice as likely to end their lives as those who have jobs. In the United States, the suicide rate, which had slowly risen since 2000, jumped during and after the 2007-9 recession. In a new book, we estimate that 4,750 “excess” suicides — that is, deaths above what pre-existing trends would predict — occurred from 2007 to 2010. Rates of such suicides were significantly greater in the states that experienced the greatest job losses. Deaths from suicide overtook deaths from car crashes in 2009. If suicides were an unavoidable consequence of economic downturns, this would just be another story about the human toll of the Great Recession. But it isn’t so. Countries that slashed health and social protection budgets, like Greece, Italy and Spain, have seen starkly worse health outcomes than nations like Germany, Iceland and Sweden, which maintained their social safety nets and opted for stimulus over austerity. (Germany preaches the virtues of austerity — for others.) As scholars of public health and political economy, we have watched aghast as politicians endlessly debate debts and deficits with little regard for the human costs of their decisions. Over the past decade, we mined huge data sets from across the globe to understand how economic shocks — from the Great Depression to the end of the Soviet Union to the Asian financial crisis to the Great Recession — affect our health. What we’ve found is that people do not inevitably get sick or die because the economy has faltered. Fiscal policy, it turns out, can be a matter of life or death. At one extreme is Greece, which is in the middle of a public health disaster. The national health budget has been cut by 40 percent since 2008, partly to meet deficit-reduction targets set by the so-called troika — the International Monetary Fund, the European Commission and the European Central Bank — as part of a 2010 austerity package. Some 35,000 doctors, nurses and other health workers have lost their jobs. Hospital admissions have soared after Greeks avoided getting routine and preventive treatment because of long wait times and rising drug costs. Infant mortality rose by 40 percent. New H.I.V. infections more than doubled, a result of rising intravenous drug use — as the budget for needle-exchange programs was cut. After mosquito-spraying programs were slashed in southern Greece, malaria cases were reported in significant numbers for the first time since the early 1970s.

In contrast, Iceland avoided a public health disaster even though it experienced, in 2008, the largest banking crisis in history, relative to the size of its economy. After three main commercial banks failed, total debt soared, unemployment increased ninefold, and the value of its currency, the krona, collapsed. Iceland became the first European country to seek an I.M.F. bailout since 1976. But instead of bailing out the banks and slashing budgets, as the I.M.F. demanded, Iceland’s politicians took a radical step: they put austerity to a vote. In two referendums, in 2010 and 2011, Icelanders voted overwhelmingly to pay off foreign creditors gradually, rather than all at once through austerity. Iceland’s economy has largely recovered, while Greece’s teeters on collapse. No one lost health care coverage or access to medication, even as the price of imported drugs rose. There was no significant increase in suicide. Last year, the first U.N. World Happiness Report ranked Iceland as one of the world’s happiest nations. Skeptics will point to structural differences between Greece and Iceland. Greece’s membership in the euro zone made currency devaluation impossible, and it had less political room to reject I.M.F. calls for austerity. But the contrast supports our thesis that an economic crisis does not necessarily have to involve a public health crisis. Somewhere between these extremes is the United States. Initially, the 2009 stimulus package shored up the safety net. But there are warning signs — beyond the higher suicide rate — that health trends are worsening. Prescriptions for antidepressants have soared. Three-quarters of a million people (particularly out-of-work young men) have turned to binge drinking. Over five million Americans lost access to health care in the recession because they lost their jobs (and either could not afford to extend their insurance under the Cobra law or exhausted their eligibility). Preventive medical visits dropped as people delayed medical care and ended up in emergency rooms. (President Obama’s health care law expands coverage, but only gradually.) The $85 billion “sequester” that began on March 1 will cut nutrition subsidies for approximately 600,000 pregnant women, newborns and infants by year’s end. Public housing budgets will be cut by nearly $2 billion this year, even while 1.4 million homes are in foreclosure. Even the budget of the Centers for Disease Control and Prevention, the nation’s main defense against epidemics like last year’s fungal meningitis outbreak, is being cut, by at least $18 million. To test our hypothesis that austerity is deadly, we’ve analyzed data from other regions and eras. After the Soviet Union dissolved, in 1991, Russia’s economy collapsed. Poverty soared and life expectancy dropped, particularly among young, working-age men. But this did not occur everywhere in the former Soviet sphere. Russia, Kazakhstan and the Baltic States (Estonia, Latvia and Lithuania) — which adopted economic “shock therapy” programs advocated by economists like Jeffrey D. Sachs and Lawrence H. Summers — experienced the worst rises in suicides, heart attacks and alcohol-related deaths.

Police protect bank from graffiti artists

Countries like Belarus, Poland and Slovenia took a different, gradualist approach, advocated by economists like Joseph E. Stiglitz and the former Soviet leader Mikhail S. Gorbachev. These countries privatized their state-controlled economies in stages and saw much better health outcomes than nearby countries that opted for mass privatizations and layoffs, which caused severe economic and social disruptions. Like the fall of the Soviet Union, the 1997 Asian financial crisis offers case studies — in effect, a natural experiment — worth examining. Thailand and Indonesia, which submitted to harsh austerity plans imposed by the I.M.F., experienced mass hunger and sharp increases in deaths from infectious disease, while Malaysia, which resisted the I.M.F.’s advice, maintained the health of its citizens. In 2012, the I.M.F. formally apologized for its handling of the crisis, estimating that the damage from its recommendations may have been three times greater than previously assumed. America’s experience of the Depression is also instructive. During the Depression, mortality rates in the United States fell by about 10 percent. The suicide rate actually soared between 1929, when the stock market crashed, and 1932, when Franklin D. Roosevelt was elected president. But the increase in suicides was more than offset by the “epidemiological transition” — improvements in hygiene that reduced deaths from infectious diseases like tuberculosis, pneumonia and influenza — and by a sharp drop in fatal traffic accidents, as Americans could not afford to drive. Comparing historical data across states, we estimate that every $100 in New Deal spending per capita was associated with a decline in pneumonia deaths of 18 per 100,000 people; a reduction in infant deaths of 18 per 1,000 live births; and a drop in suicides of 4 per 100,000 people. Our research suggests that investing $1 in public health programs can yield as much as $3 in economic growth. Public health investment not only saves lives in a recession, but can help spur economic recovery. These findings suggest that three principles should guide responses to economic crises. First, do no harm: if austerity were tested like a medication in a clinical trial, it would have been stopped long ago, given its deadly side effects. Each nation should establish a nonpartisan, independent Office of Health Responsibility, staffed by epidemiologists and economists, to evaluate the health effects of fiscal and monetary policies. Second, treat joblessness like the pandemic it is. Unemployment is a leading cause of depression, anxiety, alcoholism and suicidal thinking. Politicians in Finland and Sweden helped prevent depression and suicides during recessions by investing in “active labor-market programs” that targeted the newly unemployed and helped them find jobs quickly, with net economic benefits. Finally, expand investments in public health when times are bad. The cliché that an ounce of prevention is worth a pound of cure happens to be true. It is far more expensive to control an epidemic than to prevent one. New York City spent $1 billion in the mid-1990s to control an outbreak of drug-resistant tuberculosis. The drug-resistant strain resulted from the city’s failure to ensure that low-income tuberculosis patients completed their regimen of inexpensive generic medications. One need not be an economic ideologue — we certainly aren’t — to recognize that the price of austerity can be calculated in human lives. We are not exonerating poor policy decisions of the past or calling for universal debt forgiveness. It’s up to policy makers in America and Europe to figure out the right mix of fiscal and monetary policy. What we have found is that austerity — severe, immediate, indiscriminate cuts to social and health spending — is not only self-defeating, but fatal.”

The Excel coding error

BAD MATH

http://newyorker.com/online/blogs/comment/2012/12/austerity-economics-doesnt-work.html

http://nextnewdeal.net/rortybomb/researchers-finally-replicated-reinhart-rogoff-and-there-are-serious-problems

http://theatlantic.com/business/archive/2013/04/who-is-defending-austerity-now/275200/

Who Is Defending Austerity Now?

The Excel error heard ’round the world has deficit-cutters backpedaling

by Matthew O’Brien / 2013-04-22

“Austerians have had their worst week since the last time GDP numbers came out for a country that’s tried austerity. But this time is, well, different. It’s not “just” that southern Europe is stuck in a depression and Britain is stuck in a no-growth trap. It’s that the very intellectual foundations of austerity are unraveling. In other words, economists are finding out that austerity doesn’t work in practice or in theory. What a difference an Excel coding error makes. Austerity has been a policy in search of a justification ever since it began in 2010. Back then, policymakers decided it was time for policy to go back to “normal” even though the economy hadn’t, because deficits just felt too big. The only thing they needed was a theory telling them why what they were doing made sense. Of course, this wasn’t easy when unemployment was still high, and interest rates couldn’t go any lower. Alberto Alesina and Silvia Ardagna took the first stab at it, arguing that reducing deficits would increase confidence and growth in the short-run. But this had the defect of being demonstrably untrue (in addition to being based off a naïve reading of the data). Countries that tried to aggressively cut their deficits amidst their slumps didn’t recover; they fell into even deeper slumps.

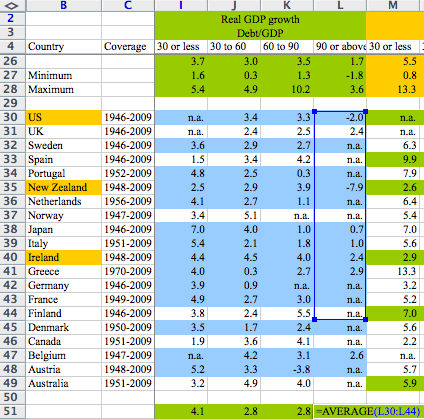

Enter Carmen Reinhart and Ken Rogoff. They gave austerity a new raison d’être by shifting the debate from the short-to-the-long-run. Reinhart and Rogoff acknowledged austerity would hurt today, but said it would help tomorrow — if it keeps governments from racking up debt of 90 percent of GDP, at which point growth supposedly slows dramatically. Now, this result was never more than just a correlation — slow growth more likely causes high debt than the reverse — but that didn’t stop policymakers from imputing totemic significance to it. That is, it became a “fact” that everybody who mattered knew was true. Except it wasn’t. Reinhart and Rogoff goofed. They accidentally excluded some data in one case, and used some wrong data in another; the former because of an Excel snafu. If you correct for these very basic errors, their correlation gets even weaker, and the growth tipping point at 90 percent of GDP disappears. In other words, there’s no there there anymore. Austerity is back to being a policy without a justification. Not only that, but, as Paul Krugman points out, Reinhart and Rogoff’s spreadsheet misadventure has been a kind of the-austerians-have-no-clothes moment. It’s been enough that even some rather unusual suspects have turned against cutting deficits now. For one, Stanford professor John Taylor claims L’affaire Excel is why the G20, the birthplace of the global austerity movement in 2010, was more muted on fiscal targets recently.

The discovery of errors in the Reinhart-Rogoff paper on the growth-debt nexus is already impacting policy. A participant in last Friday’s G20 meetings told me that the error was a factor in the decision to omit specific deficit or debt-to-GDP targets in the G20 communique.

For another, Bill Gross, the manager of the world’s largest bond fund, and who, as Joseph Cotterill of FT Alphaville points out, used to be quite the fan of British austerity, made a big about-face in an interview with the Financial Times on Monday:

The UK and almost all of Europe have erred in terms of believing that austerity, fiscal austerity in the short term, is the way to produce real growth. It is not. You’ve got to spend money.Bond investors want growth much like equity investors, and to the extent that too much austerity leads to recession or stagnation then credit spreads widen out — even if a country can print its own currency and write its own checks. In the long term it is important to be fiscal and austere. It is important to have a relatively average or low rate of debt to GDP. The question in terms of the long term and the short term is how quickly to do it.

Growth vigilantes are the new bond vigilantes. Gross thinks the boom, not the slump, is the time for austerity — which sounds an awful lot like you-know-who. The austerity fever has even broken in Europe. At least a bit. Now, eurocrats can’t say that austerity has been anything other than the best of all economic policies, but they can loosen the fiscal noose. And that’s what they might be doing, by giving countries more time and latitude to hit their deficit targets. Here’s how European Commission president José Manuel Barroso framed the issue on Monday:

While [austerity] is fundamentally right, I think it has reached its limits in many aspects. A policy to be successful not only has to be properly designed. It has to have the minimum of political and social support.

That’s not much, but it’s still much better than the growth-through-austerity plan Eurogroup president Jeroen Dijsselbloem was peddling on … Saturday. Now, Reinhart and Rogoff’s Excel imbroglio hasn’t exactly set off a new Keynesian moment. Governments aren’t going to suddenly take advantage of zero interest rates to start spending more to put people back to work. Stimulus is still a four-letter word. Indeed, the euro zone, Britain, and, to a lesser extent, the United States, are still focussed on reducing deficits above all else. But there’s a greater recognition that trying to cut deficits isn’t enough to cut debt burdens. You need growth too. In other words, people are remembering that there’s a denominator in the debt-to-GDP ratio. But austerity doesn’t just have a math problem. It has an image problem too. Just a week ago, Reinhart and Rogoff’s work was the one commandment of austerity: Thou shall not run up debt in excess of 90 percent of GDP. Wisdom didn’t get more conventional. What did this matter? Well, as Keynes famously observed, it’s better for reputation to fail conventionally than to succeed unconventionally. In other words, elites were happy to pursue obviously failed policies as long as they were the right failed policies. But now austerity doesn’t look so conventional. It looks like the punchline of a bad joke about Excel destroying the global economy. Maybe, just maybe, that will be enough to free us from some defunct economics.”