SLAVE BACKED SECURITIES

http://slaveryinnewyork.org/about_exhibit

https://theroot.com/how-slave-labor-made-new-york

https://theguardian.com/jp-morgan-apologizes-for-slaves

https://marketplace.org/parallels-between-modern-accounting-business-slavery

https://forbes.com/americas-first-bond-market-was-backed-by-enslaved-humans

America’s First Bond Market Was Backed By Enslaved Human Beings

by Pedro Nicolaci da Costa / Sep 1, 2019

“America’s first bond market was backed by a most macabre form of collateral: human beings, kidnapped from Africa and tortured into forced labor. That would have been a useful thing to know when I started my journalism career as a news assistant on the Reuters bond markets desk back in 2001. But I have only learned it now, 18 years later, thanks to the New York Times’ breathtaking 1619 Project, led by Nicole Hannah-Jones.

A piece by Princeton sociologist Matthew Desmond draws a direct and deeply compelling connection between today’s massive global market for bonds backed by everything from mortgages to lottery tickets to the U.S. economy’s slavery-founded beginnings. “Enslaved people were used as collateral for mortgages centuries before the home mortgage became the defining characteristic of middle America,” Desmond writes. “In colonial times, when land was not worth much and banks didn’t exist, most lending was based on human property.” He adds that “many Americans were first exposed to the concept of a mortgage by trafficking in enslaved people, not real estate.”

Since vivid acts of statue destruction are driving countries to reckon with their dark past, it’s much advisable to read this magnificent @nybooks piece explaining the role of American elite universities in directly enabling the enterprise of slavery.https://t.co/FttAAOpG8w

— Hassaan Chaudhary (@Hassaan06) June 12, 2020

The degree of deadly “sophistication” in this ruthless system was a testament to its premeditated and organized nature. This was already a globalized, if all-too-primitive, financial system. “Global financial markets got in on the action,” Desmond says. “When Thomas Jefferson mortgaged his enslaved workers, it was a Dutch firm that put up the collateral. […] Most of the credit “powering the American slave economy came from the London money market.”

Now, why would any of this mind-blowing history been useful when I was reporting on financial markets in the early 2000s? For starters, it would have made me a better human being. More to the point, as Desmond notes, some of the same mechanics were at work then as underpinned the slave-based economy. “Consider a Wall Street instrument as modern sounding as collateralized debt obligations or CDOs, those ticking time bombs backed by inflated home prices in the 2000s,” he writes. “CDOs were the grandchildren of mortgage backed securities based on the value of enslaved people in the 1820s and 1830s.”

The similarity doesn’t end there: “Each product created massive fortunes for the few before blowing up the economy.” Put another way, today’s mighty bond market, a formidable force on Wall Street and in world affairs, was born quite literally of human bondage. Every trader should know that. So should every student of finance. Alas, we are not there yet.”

LONG LIVED CAPITAL ASSETS

https://ucl.ac.uk/lbs/legacies

https://slate.com/empire-of-cotton-a-global-history-of-capitalism

https://bloomberg.com/the-city-of-london-has-a-slavery-problem

https://theguardian.com/britain-pro-slavery-british-history-abolition

https://theguardian.com/bank-of-england-apologises-for-slave-trade

https://nytimes.com/2019/podcasts/1619-slavery-cotton-capitalism.html

https://nytimes.com/interactive/2019/08/14/magazine/slavery-capitalism.html

In order to understand the brutality of American capitalism, start on the plantation

by Matthew Desmond / August 14, 2019

“This is a capitalist society. It’s a fatalistic mantra that seems to get repeated to anyone who questions why America can’t be more fair or equal. But around the world, there are many types of capitalist societies, ranging from liberating to exploitative, protective to abusive, democratic to unregulated. When Americans declare that “we live in a capitalist society” — as a real estate mogul told The Miami Herald last year when explaining his feelings about small-business owners being evicted from their Little Haiti storefronts — what they’re often defending is our nation’s peculiarly brutal economy.

“Low-road capitalism,” the University of Wisconsin-Madison sociologist Joel Rogers has called it. In a capitalist society that goes low, wages are depressed as businesses compete over the price, not the quality, of goods; so-called unskilled workers are typically incentivized through punishments, not promotions; inequality reigns and poverty spreads. In the United States, the richest 1 percent of Americans own 40 percent of the country’s wealth, while a larger share of working-age people (18-65) live in poverty than in any other nation belonging to the Organization for Economic Cooperation and Development (O.E.C.D.).

https://twitter.com/ProfMoryl/status/1268955377628057601

Or consider worker rights in different capitalist nations. In Iceland, 90 percent of wage and salaried workers belong to trade unions authorized to fight for living wages and fair working conditions. Thirty-four percent of Italian workers are unionized, as are 26 percent of Canadian workers. Only 10 percent of American wage and salaried workers carry union cards. The O.E.C.D. scores nations along a number of indicators, such as how countries regulate temporary work arrangements. Scores run from 5 (“very strict”) to 1 (“very loose”). Brazil scores 4.1 and Thailand, 3.7, signaling toothy regulations on temp work. Further down the list are Norway (3.4), India (2.5) and Japan (1.3). The United States scored 0.3, tied for second to last place with Malaysia. How easy is it to fire workers?

Countries like Indonesia (4.1) and Portugal (3) have strong rules about severance pay and reasons for dismissal. Those rules relax somewhat in places like Denmark (2.1) and Mexico (1.9). They virtually disappear in the United States, ranked dead last out of 71 nations with a score of 0.5. Those searching for reasons the American economy is uniquely severe and unbridled have found answers in many places (religion, politics, culture). But recently, historians have pointed persuasively to the gnatty fields of Georgia and Alabama, to the cotton houses and slave auction blocks, as the birthplace of America’s low-road approach to capitalism.

Slavery was undeniably a font of phenomenal wealth. By the eve of the Civil War, the Mississippi Valley was home to more millionaires per capita than anywhere else in the United States. Cotton grown and picked by enslaved workers was the nation’s most valuable export. The combined value of enslaved people exceeded that of all the railroads and factories in the nation. New Orleans boasted a denser concentration of banking capital than New York City. What made the cotton economy boom in the United States, and not in all the other far-flung parts of the world with climates and soil suitable to the crop, was our nation’s unflinching willingness to use violence on nonwhite people and to exert its will on seemingly endless supplies of land and labor. Given the choice between modernity and barbarism, prosperity and poverty, lawfulness and cruelty, democracy and totalitarianism, America chose all of the above.

Nearly two average American lifetimes (79 years) have passed since the end of slavery, only two. It is not surprising that we can still feel the looming presence of this institution, which helped turn a poor, fledgling nation into a financial colossus. The surprising bit has to do with the many eerily specific ways slavery can still be felt in our economic life. “American slavery is necessarily imprinted on the DNA of American capitalism,” write the historians Sven Beckert and Seth Rockman. The task now, they argue, is “cataloging the dominant and recessive traits” that have been passed down to us, tracing the unsettling and often unrecognized lines of descent by which America’s national sin is now being visited upon the third and fourth generations.

They picked inlong rows, bent bodies shuffling through cotton fields white in bloom. Men, women and children picked, using both hands to hurry the work. Some picked in Negro cloth, their raw product returning to them by way of New England mills. Some picked completely naked. Young children ran water across the humped rows, while overseers peered down from horses. Enslaved workers placed each cotton boll into a sack slung around their necks. Their haul would be weighed after the sunlight stalked away from the fields and, as the freedman Charles Ball recalled, you couldn’t “distinguish the weeds from the cotton plants.” If the haul came up light, enslaved workers were often whipped. “A short day’s work was always punished,” Ball wrote.

Cotton was to the 19th century what oil was to the 20th: among the world’s most widely traded commodities. Cotton is everywhere, in our clothes, hospitals, soap. Before the industrialization of cotton, people wore expensive clothes made of wool or linen and dressed their beds in furs or straw. Whoever mastered cotton could make a killing. But cotton needed land. A field could only tolerate a few straight years of the crop before its soil became depleted. Planters watched as acres that had initially produced 1,000 pounds of cotton yielded only 400 a few seasons later. The thirst for new farmland grew even more intense after the invention of the cotton gin in the early 1790s. Before the gin, enslaved workers grew more cotton than they could clean. The gin broke the bottleneck, making it possible to clean as much cotton as you could grow.

The United States solved its land shortage by expropriating millions of acres from Native Americans, often with military force, acquiring Georgia, Alabama, Tennessee and Florida. It then sold that land on the cheap — just $1.25 an acre in the early 1830s ($38 in today’s dollars) — to white settlers. Naturally, the first to cash in were the land speculators. Companies operating in Mississippi flipped land, selling it soon after purchase, commonly for double the price. Enslaved workers felled trees by ax, burned the underbrush and leveled the earth for planting.

“Whole forests were literally dragged out by the roots,” John Parker, an enslaved worker, remembered. A lush, twisted mass of vegetation was replaced by a single crop. An origin of American money exerting its will on the earth, spoiling the environment for profit, is found in the cotton plantation. Floods became bigger and more common. The lack of biodiversity exhausted the soil and, to quote the historian Walter Johnson, “rendered one of the richest agricultural regions of the earth dependent on upriver trade for food.”

As slave labor camps spread throughout the South, production surged. By 1831, the country was delivering nearly half the world’s raw cotton crop, with 350 million pounds picked that year. Just four years later, it harvested 500 million pounds. Southern white elites grew rich, as did their counterparts in the North, who erected textile mills to form, in the words of the Massachusetts senator Charles Sumner, an “unhallowed alliance between the lords of the lash and the lords of the loom.” The large-scale cultivation of cotton hastened the invention of the factory, an institution that propelled the Industrial Revolution and changed the course of history.

In 1810, there were 87,000 cotton spindles in America. Fifty years later, there were five million. Slavery, wrote one of its defenders in De Bow’s Review, a widely read agricultural magazine, was the “nursing mother of the prosperity of the North.” Cotton planters, millers and consumers were fashioning a new economy, one that was global in scope and required the movement of capital, labor and products across long distances. In other words, they were fashioning a capitalist economy. “The beating heart of this new system,” Beckert writes, “was slavery.”

Perhaps you’re reading this at work, maybe at a multinational corporation that runs like a soft-purring engine. You report to someone, and someone reports to you. Everything is tracked, recorded and analyzed, via vertical reporting systems, double-entry record-keeping and precise quantification. Data seems to hold sway over every operation. It feels like a cutting-edge approach to management, but many of these techniques that we now take for granted were developed by and for large plantations.

When an accountant depreciates an asset to save on taxes or when a midlevel manager spends an afternoon filling in rows and columns on an Excel spreadsheet, they are repeating business procedures whose roots twist back to slave-labor camps. And yet, despite this, “slavery plays almost no role in histories of management,” notes the historian Caitlin Rosenthal in her book “Accounting for Slavery.”

Since the 1977 publication of Alfred Chandler’s classic study, “The Visible Hand,” historians have tended to connect the development of modern business practices to the 19th-century railroad industry, viewing plantation slavery as precapitalistic, even primitive. It’s a more comforting origin story, one that protects the idea that America’s economic ascendancy developed not because of, but in spite of, millions of black people toiling on plantations. But management techniques used by 19th-century corporations were implemented during the previous century by plantation owners.

Planters aggressively expanded their operations to capitalize on economies of scale inherent to cotton growing, buying more enslaved workers, investing in large gins and presses and experimenting with different seed varieties. To do so, they developed complicated workplace hierarchies that combined a central office, made up of owners and lawyers in charge of capital allocation and long-term strategy, with several divisional units, responsible for different operations.

Rosenthal writes of one plantation where the owner supervised a top lawyer, who supervised another lawyer, who supervised an overseer, who supervised three bookkeepers, who supervised 16 enslaved head drivers and specialists (like bricklayers), who supervised hundreds of enslaved workers. Everyone was accountable to someone else, and plantations pumped out not just cotton bales but volumes of data about how each bale was produced. This organizational form was very advanced for its time, displaying a level of hierarchal complexity equaled only by large government structures, like that of the British Royal Navy.

Like today’s titans of industry, planters understood that their profits climbed when they extracted maximum effort out of each worker. So they paid close attention to inputs and outputs by developing precise systems of record-keeping. Meticulous bookkeepers and overseers were just as important to the productivity of a slave-labor camp as field hands. Plantation entrepreneurs developed spreadsheets, like Thomas Affleck’s “Plantation Record and Account Book,” which ran into eight editions circulated until the Civil War. Affleck’s book was a one-stop-shop accounting manual, complete with rows and columns that tracked per-worker productivity. This book “was really at the cutting edge of the informational technologies available to businesses during this period,” Rosenthal told me.

“I have never found anything remotely as complex as Affleck’s book for free labor.” Enslavers used the book to determine end-of-the-year balances, tallying expenses and revenues and noting the causes of their biggest gains and losses. They quantified capital costs on their land, tools and enslaved workforces, applying Affleck’s recommended interest rate. Perhaps most remarkable, they also developed ways to calculate depreciation, a breakthrough in modern management procedures, by assessing the market value of enslaved workers over their life spans. Values generally peaked between the prime ages of 20 and 40 but were individually adjusted up or down based on sex, strength and temperament: people reduced to data points.

This level of data analysis also allowed planters to anticipate rebellion. Tools were accounted for on a regular basis to make sure a large number of axes or other potential weapons didn’t suddenly go missing. “Never allow any slave to lock or unlock any door,” advised a Virginia enslaver in 1847. In this way, new bookkeeping techniques developed to maximize returns also helped to ensure that violence flowed in one direction, allowing a minority of whites to control a much larger group of enslaved black people. American planters never forgot what happened in Saint-Domingue (now Haiti) in 1791, when enslaved workers took up arms and revolted. In fact, many white enslavers overthrown during the Haitian Revolution relocated to the United States and started over.

Overseers recorded each enslaved worker’s yield. Accountings took place not only after nightfall, when cotton baskets were weighed, but throughout the workday. In the words of a North Carolina planter, enslaved workers were to be “followed up from day break until dark.” Having hands line-pick in rows sometimes longer than five football fields allowed overseers to spot anyone lagging behind. The uniform layout of the land had a logic; a logic designed to dominate. Faster workers were placed at the head of the line, which encouraged those who followed to match the captain’s pace. When enslaved workers grew ill or old, or became pregnant, they were assigned to lighter tasks.

One enslaver established a “sucklers gang” for nursing mothers, as well as a “measles gang,” which at once quarantined those struck by the virus and ensured that they did their part to contribute to the productivity machine. Bodies and tasks were aligned with rigorous exactitude. In trade magazines, owners swapped advice about the minutiae of planting, including slave diets and clothing as well as the kind of tone a master should use. In 1846, one Alabama planter advised his fellow enslavers to always give orders “in a mild tone, and try to leave the impression on the mind of the negro that what you say is the result of reflection.” The devil (and his profits) were in the details.

The uncompromising pursuit of measurement and scientific accounting displayed in slave plantations predates industrialism. Northern factories would not begin adopting these techniques until decades after the Emancipation Proclamation. As the large slave-labor camps grew increasingly efficient, enslaved black people became America’s first modern workers, their productivity increasing at an astonishing pace. During the 60 years leading up to the Civil War, the daily amount of cotton picked per enslaved worker increased 2.3 percent a year. That means that in 1862, the average enslaved fieldworker picked not 25 percent or 50 percent as much but 400 percent as much cotton than his or her counterpart did in 1801.

Today modern technology has facilitated unremitting workplace supervision, particularly in the service sector. Companies have developed software that records workers’ keystrokes and mouse clicks, along with randomly capturing screenshots multiple times a day. Modern-day workers are subjected to a wide variety of surveillance strategies, from drug tests and closed-circuit video monitoring to tracking apps and even devices that sense heat and motion. A 2006 survey found that more than a third of companies with work forces of 1,000 or more had staff members who read through employees’ outbound emails. The technology that accompanies this workplace supervision can make it feel futuristic. But it’s only the technology that’s new. The core impulse behind that technology pervaded plantations, which sought innermost control over the bodies of their enslaved work force.

The cotton plantation was America’s first big business, and the nation’s first corporate Big Brother was the overseer. And behind every cold calculation, every rational fine-tuning of the system, violence lurked. Plantation owners used a combination of incentives and punishments to squeeze as much as possible out of enslaved workers. Some beaten workers passed out from the pain and woke up vomiting. Some “danced” or “trembled” with every hit. An 1829 first-person account from Alabama recorded an overseer’s shoving the faces of women he thought had picked too slow into their cotton baskets and opening up their backs. To the historian Edward Baptist, before the Civil War, Americans “lived in an economy whose bottom gear was torture.”

There is some comfort, I think, in attributing the sheer brutality of slavery to dumb racism. We imagine pain being inflicted somewhat at random, doled out by the stereotypical white overseer, free but poor. But a good many overseers weren’t allowed to whip at will. Punishments were authorized by the higher-ups. It was not so much the rage of the poor white Southerner but the greed of the rich white planter that drove the lash. The violence was neither arbitrary nor gratuitous. It was rational, capitalistic, all part of the plantation’s design.

“Each individual having a stated number of pounds of cotton to pick,” a formerly enslaved worker, Henry Watson, wrote in 1848, “the deficit of which was made up by as many lashes being applied to the poor slave’s back.” Because overseers closely monitored enslaved workers’ picking abilities, they assigned each worker a unique quota. Falling short of that quota could get you beaten, but overshooting your target could bring misery the next day, because the master might respond by raising your picking rate.

Profits from heightened productivity were harnessed through the anguish of the enslaved. This was why the fastest cotton pickers were often whipped the most. It was why punishments rose and fell with global market fluctuations. Speaking of cotton in 1854, the fugitive slave John Brown remembered, “When the price rises in the English market, the poor slaves immediately feel the effects, for they are harder driven, and the whip is kept more constantly going.” Unrestrained capitalism holds no monopoly on violence, but in making possible the pursuit of near limitless personal fortunes, often at someone else’s expense, it does put a cash value on our moral commitments.

Slavery did supplement white workers with what W.E.B. Du Bois called a “public and psychological wage,” which allowed them to roam freely and feel a sense of entitlement. But this, too, served the interests of money. Slavery pulled down all workers’ wages. Both in the cities and countryside, employers had access to a large and flexible labor pool made up of enslaved and free people. Just as in today’s gig economy, day laborers during slavery’s reign often lived under conditions of scarcity and uncertainty, and jobs meant to be worked for a few months were worked for lifetimes. Labor power had little chance when the bosses could choose between buying people, renting them, contracting indentured servants, taking on apprentices or hiring children and prisoners.

This not only created a starkly uneven playing field, dividing workers from themselves; it also made “all nonslavery appear as freedom,” as the economic historian Stanley Engerman has written. Witnessing the horrors of slavery drilled into poor white workers that things could be worse. So they generally accepted their lot, and American freedom became broadly defined as the opposite of bondage. It was a freedom that understood what it was against but not what it was for; a malnourished and mean kind of freedom that kept you out of chains but did not provide bread or shelter. It was a freedom far too easily pleased.

In recent decades, America has experienced the financialization of its economy. In 1980, Congress repealed regulations that had been in place since the 1933 Glass-Steagall Act, allowing banks to merge and charge their customers higher interest rates. Since then, increasingly profits have accrued not by trading and producing goods and services but through financial instruments. Between 1980 and 2008, more than $6.6 trillion was transferred to financial firms.

After witnessing the successes and excesses of Wall Street, even nonfinancial companies began finding ways to make money from financial products and activities. Ever wonder why every major retail store, hotel chain and airline wants to sell you a credit card? This financial turn has trickled down into our everyday lives: It’s there in our pensions, home mortgages, lines of credit and college-savings portfolios. Americans with some means now act like “enterprising subjects,” in the words of the political scientist Robert Aitken.

As it’s usually narrated, the story of the ascendancy of American finance tends to begin in 1980, with the gutting of Glass-Steagall, or in 1944 with Bretton Woods, or perhaps in the reckless speculation of the 1920s. But in reality, the story begins during slavery. Consider, for example, one of the most popular mainstream financial instruments: the mortgage.

Enslaved people were used as collateral for mortgages centuries before the home mortgage became the defining characteristic of middle America. In colonial times, when land was not worth much and banks didn’t exist, most lending was based on human property. In the early 1700s, slaves were the dominant collateral in South Carolina.

Many Americans were first exposed to the concept of a mortgage by trafficking in enslaved people, not real estate, and “the extension of mortgages to slave property helped fuel the development of American (and global) capitalism,” the historian Joshua Rothman told me. Or consider a Wall Street financial instrument as modern-sounding as collateralized debt obligations (C.D.O.s), those ticking time bombs backed by inflated home prices in the 2000s. C.D.O.s were the grandchildren of mortgage-backed securities based on the inflated value of enslaved people sold in the 1820s and 1830s. Each product created massive fortunes for the few before blowing up the economy.

Enslavers were not the first ones to securitize assets and debts in America. The land companies that thrived during the late 1700s relied on this technique, for instance. But enslavers did make use of securities to such an enormous degree for their time, exposing stakeholders throughout the Western world to enough risk to compromise the world economy, that the historian Edward Baptist told me that this can be viewed as “a new moment in international capitalism, where you are seeing the development of a globalized financial market.”

The novel thing about the 2008 foreclosure crisis was not the concept of foreclosing on a homeowner but foreclosing on millions of them. Similarly, what was new about securitizing enslaved people in the first half of the 19th century was not the concept of securitization itself but the crazed level of rash speculation on cotton that selling slave debt promoted. As America’s cotton sector expanded, the value of enslaved workers soared. Between 1804 and 1860, the average price of men ages 21 to 38 sold in New Orleans grew to $1,200 from roughly $450. Because they couldn’t expand their cotton empires without more enslaved workers, ambitious planters needed to find a way to raise enough capital to purchase more hands.

Enter the banks. The Second Bank of the United States, chartered in 1816, began investing heavily in cotton. In the early 1830s, the slaveholding Southwestern states took almost half the bank’s business. Around the same time, state-chartered banks began multiplying to such a degree that one historian called it an “orgy of bank-creation.”

When seeking loans, planters used enslaved people as collateral. Thomas Jefferson mortgaged 150 of his enslaved workers to build Monticello. People could be sold much more easily than land, and in multiple Southern states, more than eight in 10 mortgage-secured loans used enslaved people as full or partial collateral. As the historian Bonnie Martin has written, “slave owners worked their slaves financially, as well as physically from colonial days until emancipation” by mortgaging people to buy more people. Access to credit grew faster than Mississippi kudzu, leading one 1836 observer to remark that in cotton country “money, or what passed for money, was the only cheap thing to be had.”

Planters took on immense amounts of debt to finance their operations. Why wouldn’t they? The math worked out. A cotton plantation in the first decade of the 19th century could leverage their enslaved workers at 8 percent interest and record a return three times that. So leverage they did, sometimes volunteering the same enslaved workers for multiple mortgages. Banks lent with little restraint. By 1833, Mississippi banks had issued 20 times as much paper money as they had gold in their coffers. In several Southern counties, slave mortgages injected more capital into the economy than sales from the crops harvested by enslaved workers.

Global financial markets got in on the action. When Thomas Jefferson mortgaged his enslaved workers, it was a Dutch firm that put up the money. The Louisiana Purchase, which opened millions of acres to cotton production, was financed by Baring Brothers, the well-heeled British commercial bank. A majority of credit powering the American slave economy came from the London money market.

Years after abolishing the African slave trade in 1807, Britain, and much of Europe along with it, was bankrolling slavery in the United States. To raise capital, state-chartered banks pooled debt generated by slave mortgages and repackaged it as bonds promising investors annual interest. During slavery’s boom time, banks did swift business in bonds, finding buyers in Hamburg and Amsterdam, in Boston and Philadelphia.

Some historians have claimed that the British abolition of the slave trade was a turning point in modernity, marked by the development of a new kind of moral consciousness when people began considering the suffering of others thousands of miles away. But perhaps all that changed was a growing need to scrub the blood of enslaved workers off American dollars, British pounds and French francs, a need that Western financial markets fast found a way to satisfy through the global trade in bank bonds. Here was a means to profit from slavery without getting your hands dirty.

In fact, many investors may not have realized that their money was being used to buy and exploit people, just as many of us who are vested in multinational textile companies today are unaware that our money subsidizes a business that continues to rely on forced labor in countries like Uzbekistan and China and child workers in countries like India and Brazil. Call it irony, coincidence or maybe cause — historians haven’t settled the matter — but avenues to profit indirectly from slavery grew in popularity as the institution of slavery itself grew more unpopular. “I think they go together,” the historian Calvin Schermerhorn told me. “We care about fellow members of humanity, but what do we do when we want returns on an investment that depends on their bound labor?” he said. “Yes, there is a higher consciousness. But then it comes down to: Where do you get your cotton from?”

Banks issued tens of millions of dollars in loans on the assumption that rising cotton prices would go on forever. Speculation reached a fever pitch in the 1830s, as businessmen, planters and lawyers convinced themselves that they could amass real treasure by joining in a risky game that everyone seemed to be playing. If planters thought themselves invincible, able to bend the laws of finance to their will, it was most likely because they had been granted authority to bend the laws of nature to their will, to do with the land and the people who worked it as they pleased. Du Bois wrote: “The mere fact that a man could be, under the law, the actual master of the mind and body of human beings had to have disastrous effects. It tended to inflate the ego of most planters beyond all reason; they became arrogant, strutting, quarrelsome kinglets.” What are the laws of economics to those exercising godlike power over an entire people?

We know how these stories end. The American South rashly overproduced cotton thanks to an abundance of cheap land, labor and credit, consumer demand couldn’t keep up with supply, and prices fell. The value of cotton started to drop as early as 1834 before plunging like a bird winged in midflight, setting off the Panic of 1837. Investors and creditors called in their debts, but plantation owners were underwater. Mississippi planters owed the banks in New Orleans $33 million in a year their crops yielded only $10 million in revenue. They couldn’t simply liquidate their assets to raise the money. When the price of cotton tumbled, it pulled down the value of enslaved workers and land along with it. People bought for $2,000 were now selling for $60. Today, we would say the planters’ debt was “toxic.”

Because enslavers couldn’t repay their loans, the banks couldn’t make interest payments on their bonds. Shouts went up around the Western world, as investors began demanding that states raise taxes to keep their promises. After all, the bonds were backed by taxpayers. But after a swell of populist outrage, states decided not to squeeze the money out of every Southern family, coin by coin. But neither did they foreclose on defaulting plantation owners.

If they tried, planters absconded to Texas (an independent republic at the time) with their treasure and enslaved work force. Furious bondholders mounted lawsuits and cashiers committed suicide, but the bankrupt states refused to pay their debts. Cotton slavery was too big to fail. The South chose to cut itself out of the global credit market, the hand that had fed cotton expansion, rather than hold planters and their banks accountable for their negligence and avarice.

Even academic historians, who from their very first graduate course are taught to shun presentism and accept history on its own terms, haven’t been able to resist drawing parallels between the Panic of 1837 and the 2008 financial crisis. All the ingredients are there: mystifying financial instruments that hide risk while connecting bankers, investors and families around the globe; fantastic profits amassed overnight; the normalization of speculation and breathless risk-taking; stacks of paper money printed on the myth that some institution (cotton, housing) is unshakable; considered and intentional exploitation of black people; and impunity for the profiteers when it all falls apart — the borrowers were bailed out after 1837, the banks after 2008.

During slavery, “Americans built a culture of speculation unique in its abandon,” writes the historian Joshua Rothman in his 2012 book, “Flush Times and Fever Dreams.” That culture would drive cotton production up to the Civil War, and it has been a defining characteristic of American capitalism ever since. It is the culture of acquiring wealth without work, growing at all costs and abusing the powerless. It is the culture that brought us the Panic of 1837, the stock-market crash of 1929 and the recession of 2008.

It is the culture that has produced staggering inequality and undignified working conditions. If today America promotes a particular kind of low-road capitalism — a union-busting capitalism of poverty wages, gig jobs and normalized insecurity; a winner-take-all capitalism of stunning disparities not only permitting but awarding financial rule-bending; a racist capitalism that ignores the fact that slavery didn’t just deny black freedom but built white fortunes, originating the black-white wealth gap that annually grows wider— one reason is that American capitalism was founded on the lowest road there is.”

HOW SLAVERY MADE WALL STREET

by Tiya Miles

While “Main Street” might be anywhere and everywhere, as the historian Joshua Freeman points out, “Wall Street” has only ever been one specific place on the map. New York has been a principal center of American commerce dating back to the colonial period — a centrality founded on the labor extracted from thousands of indigenous American and African slaves.

Desperate for hands to build towns, work wharves, tend farms and keep households, colonists across the American Northeast — Puritans in Massachusetts Bay, Dutch settlers in New Netherland and Quakers in Pennsylvania — availed themselves of slave labor. Native Americans captured in colonial wars in New England were forced to work, and African people were imported in greater and greater numbers. New York City soon surpassed other slaving towns of the Northeast in scale as well as impact. Founded by the Dutch as New Amsterdam in 1625, what would become the City of New York first imported 11 African men in 1626.

The Dutch West India Company owned these men and their families, directing their labors to common enterprises like land clearing and road construction. After the English Duke of York acquired authority over the colony and changed its name, slavery grew harsher and more comprehensive. As the historian Leslie Harris has written, 40 percent of New York households held enslaved people in the early 1700s. New Amsterdam’s and New York’s enslaved put in place much of the local infrastructure, including Broad Way and the Bowery roads, Governors Island, and the first municipal buildings and churches. The unfree population in New York was not small, and their experience of exploitation was not brief. In 1991, construction workers uncovered an extensive 18th-century African burial ground in Lower Manhattan, the final resting place of approximately 20,000 people.

And New York City’s investment in slavery expanded in the 19th century. In 1799 the state of New York passed the first of a series of laws that would gradually abolish slavery over the coming decades, but the investors and financiers of the state’s primary metropolis doubled down on the business of slavery. New Yorkers invested heavily in the growth of Southern plantations, catching the wave of the first cotton boom. Southern planters who wanted to buy more land and black people borrowed funds from New York bankers and protected the value of bought bodies with policies from New York insurance companies.

New York factories produced the agricultural tools forced into Southern slaves’ hands and the rough fabric called “Negro Cloth” worn on their backs. Ships originating in New York docked in the port of New Orleans to service the trade in domestic and (by then, illegal) international slaves. As the historian David Quigley has demonstrated, New York City’s phenomenal economic consolidation came as a result of its dominance in the Southern cotton trade, facilitated by the construction of the Erie Canal. It was in this moment — the early decades of the 1800s — that New York City gained its status as a financial behemoth through shipping raw cotton to Europe and bankrolling the boom industry that slavery made.

In 1711, New York City officials decreed that “all Negro and Indian slaves that are let out to hire … be hired at the Market house at the Wall Street Slip.” It is uncanny, but perhaps predictable, that the original wall for which Wall Street is named was built by the enslaved at a site that served as the city’s first organized slave auction. The capital profits and financial wagers of Manhattan, the United States and the world still flow through this place where black and red people were traded and where the wealth of a region was built on slavery.

COTTON and the GLOBAL MARKET

by Mehrsa Baradaran

Cotton produced under slavery created a worldwide market that brought together the Old World and the New: the industrial textile mills of the Northern states and England, on the one hand, and the cotton plantations of the American South on the other. Textile mills in industrial centers like Lancashire, England, purchased a majority of cotton exports, which created worldwide trade hubs in London and New York where merchants could trade in, invest in, insure and speculate on the cotton—commodity market. Though trade in other commodities existed, it was cotton (and the earlier trade in slave-produced sugar from the Caribbean) that accelerated worldwide commercial markets in the 19th century, creating demand for innovative contracts, novel financial products and modern forms of insurance and credit.

Like all agricultural goods, cotton is prone to fluctuations in quality depending on crop type, location and environmental conditions. Treating it as a commodity led to unique problems: How would damages be calculated if the wrong crop was sent? How would you assure that there was no misunderstanding between two parties on time of delivery? Legal concepts we still have to this day, like “mutual mistake” (the notion that contracts can be voided if both parties relied on a mistaken assumption), were developed to deal with these issues. Textile merchants needed to purchase cotton in advance of their own production, which meant that farmers needed a way to sell goods they had not yet grown; this led to the invention of futures contracts and, arguably, the commodities markets still in use today.

From the first decades of the 1800s, during the height of the trans-Atlantic cotton trade, the sheer size of the market and the escalating number of disputes between counterparties was such that courts and lawyers began to articulate and codify the common-law standards regarding contracts. This allowed investors and traders to mitigate their risk through contractual arrangement, which smoothed the flow of goods and money. Today law students still study some of these pivotal cases as they learn doctrines like forseeability, mutual mistake and damages.

FIAT CURRENCY and the CIVIL WAR

by Mehrsa Baradaran

The Constitution is riddled with compromises made between the North and South over the issue of slavery — the Electoral College, the three-fifths clause — but paper currency was too contentious an issue for the framers, so it was left out entirely. Thomas Jefferson, like many Southerners, believed that a national currency would make the federal government too powerful and would also favor the Northern trade-based economy over the plantation economy. So, for much of its first century, the United States was without a national bank or a uniform currency, leaving its economy prone to crisis, bank runs and instability.

At the height of the war, Lincoln understood that he could not feed the troops without more money, so he issued a national currency, backed by the full faith and credit of the United States Treasury — but not by gold. (These bills were known derisively as “greenbacks,” a word that has lived on.) The South had a patchwork currency that was backed by the holdings of private banks — the same banks that helped finance the entire Southern economy, from the plantations to the people enslaved on them. Some Confederate bills even had depictions of enslaved people on their backs.

In a sense, the war over slavery was also a war over the future of the economy and the essentiality of value. By issuing fiat currency, Lincoln bet the future on the elasticity of value. This was the United States’ first formal experiment with fiat money, and it was a resounding success. The currency was accepted by national and international creditors — such as private creditors from London, Amsterdam and Paris — and funded the feeding and provisioning of Union troops. In turn, the success of the Union Army fortified the new currency. Lincoln assured critics that the move would be temporary, but leaders who followed him eventually made it permanent — first Franklin Roosevelt during the Great Depression and then, formally, Richard Nixon in 1971.

LIMITS of BANKING REGULATION

by Mehrsa Baradaran

“At the start of the Civil War, only states could charter banks. It wasn’t until the National Currency Act of 1863 and the National Bank Act of 1864 passed at the height of the Civil War that banks operated in this country on a national scale, with federal oversight. And even then, it was only law in the North. The Union passed the bills so it could establish a national currency in order to finance the war.

The legislation also created the Office of the Comptroller of the Currency (O.C.C.), the first federal bank regulator. After the war, states were allowed to keep issuing bank charters of their own. This byzantine infrastructure remains to this day and is known as the dual banking system. Among all nations in the world, only the United States has such a fragmentary, overlapping and inefficient system — a direct relic of the conflict between federal and state power over maintenance of the slave-based economy of the South.

Both state regulators and the O.C.C., one of the largest federal regulators, are funded by fees from the banks they regulate. Moreover, banks are effectively able to choose regulators — either federal or state ones, depending on their charter. They can even change regulators if they become unsatisfied with the one they’ve chosen. Consumer-protection laws, interest-rate caps and basic-soundness regulations have often been rendered ineffectual in the process — and deregulation of this sort tends to lead to crisis.

In the mid-2000s, when subprime lenders started appearing in certain low-income neighborhoods, many of them majority black and Latino, several state banking regulators took note. In Michigan, the state insurance regulator tried to enforce its consumer-protection laws on Wachovia Mortgage, a subsidiary of Wachovia Bank. In response, Wachovia’s national regulator, the O.C.C., stepped in, claiming that banks with a national charter did not have to comply with state law. The Supreme Court agreed with the O.C.C., and Wachovia continued to engage in risky subprime activity. Eventually loans like those blew up the banking system and the investments of many Americans — especially the most vulnerable. Black communities lost 53 percent of their wealth because of the crisis, a loss that a former congressman, Brad Miller, said “has almost been an extinction event.”

MARITIME SLAVE INSURANCE

https://muse.jhu.edu/article/190342

https://journals.akademicka.pl/adamericam/article/view/1098

https://cambridge.org/slave-life-insurance-policies-of-dutch-private-slave-ships

https://theguardian.com/lloyds-of-london-to-make-slave-trade-reparations

https://uk.reuters.com/lloyds-of-london-to-pay-for-atlantic-slave-trade

https://semanticscholar.org/paper/Bonded-Life-Kish-Leroy

https://nytimes.com/2002/05/05/nyregion/slave-policies

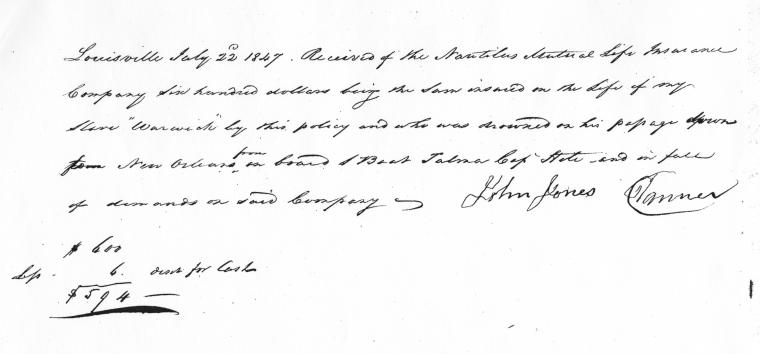

Slave Policies / by Virginia Groark / May 5, 2002

“…It’s not pleasant to talk about it today, to put it mildly, but slaves were insured just like any other thing that the farmers owned, that the slave owners owned,” said Tom Baker, director of the Insurance Law Center at the University of Connecticut School of Law. “If you were selling insurance in slave states to people who had plantations, that was one of the things that you sold. “It was very common,” he added. “Basically, insurance and slavery go all the way back as far as American history.”

Aetna, which in 2000 apologized for its involvement in slavery, is the only insurance company to be named in the slave reparations lawsuit, though one of the plaintiff’s lawyers, Roger S. Wareham, said he expected that other insurance companies would be sued. A brief examination of documents demonstrates that Aetna was hardly the only company that engaged in the practice.

“It wasn’t just the Aetna company,” said Charles L. Blockson, curator of the Charles L. Blockson Afro-American Collection at Temple University. “A lot of the old insurance companies, especially the ones that handled shipping in the Newport, R.I., area and New London.”

The problem for the plaintiffs, experts said, is that many firms are defunct, have changed names, destroyed old records, or have been absorbed by other companies. In addition, it is sometimes difficult to document ties to the slave trade. In the case of slave ships, for example, 19th-century marine insurance policies often didn’t identify the cargo on board. Instead, the policy simply stated that it insured “goods” on board. “What strikes me from what I know already is that the records do not say clearly that slaves were insured,” said Ugo Nwokeji, assistant professor of history at UConn.

“Insurance policy for slave, Warwick. (Source: NYPL Schomburg Center for Research in Black Culture, Manuscripts, Archives and Rare Books Division)”

“We cannot say that we know it was widespread, although it is well possible that it would have been widespread.” The insurance industry’s connection to slavery is not a new revelation. It has been written about in publications like Mr. Blockson’s 1977 book, “Black Genealogy.” Even on eBay, the Internet auction site, copies of slave life insurance polices are for sale. And the tale of the slave ship Zong, in which 133 sick slaves were thrown overboard in 1781 so the ship’s owners could collect insurance, has been studied for years…”

SLAVE LIFE INSURANCE

http://treasuryofwearysouls.com/map

https://nonprofitquarterly.org/the-coloring-of-risk

http://radicalcartography.net/index.html?slave_insurance

http://insurance.ca.gov/01-consumers/150-other-prog/10-seir

https://techcrunch.com/visualizing-the-slave-insurance-industry

https://foreignpolicy.com/slave-insurance-market-aetna-aig-new-york-life

https://nytimes.com/insurance-policies-on-slaves-new-york-lifes-complicated-past

Insurance Policies on Slaves: New York Life’s Complicated Past

by Rachel L. Swarns / December 18, 2016

New York Life, the nation’s third-largest life insurance company, opened in Manhattan’s financial district in the spring of 1845. The firm possessed a prime address — 58 Wall Street — and a board of trustees populated by some of the city’s wealthiest merchants, bankers and railroad magnates. Sales were sluggish that year. So the company looked south. There, in Richmond, Va., an enterprising New York Life agent sold more than 30 policies in a single day in February 1846. Soon, advertisements began appearing in newspapers from Wilmington, N.C., to Louisville as the New York-based company encouraged Southerners to buy insurance to protect their most precious commodity: their slaves. Alive, slaves were among a white man’s most prized assets. Dead, they were considered virtually worthless. Life insurance changed that calculus, allowing slave owners to recoup three-quarters of a slave’s value in the event of an untimely death.

James De Peyster Ogden, New York Life’s first president, would later describe the American system of human bondage as “evil.” But by 1847, insurance policies on slaves accounted for a third of the policies in a firm that would become one of the nation’s Fortune 100 companies. Georgetown, Harvard and other universities have drawn national attention to the legacy of slavery this year as they have acknowledged benefiting from the slave trade and grappled with how to make amends. But slavery also generated business for some of the most prominent modern-day corporations, underscoring the ties that many contemporary institutions have to this painful period of history.

[mixcloud https://www.mixcloud.com/newbooksinhistory3/sharon-ann-murphy-investing-in-life-insurance-in-antebellum-america-johns-hopkins-up-2010/ width=100% height=60 hide_cover=1 mini=1]

Banks absorbed by JPMorgan Chase and Wells Fargo allowed Southerners seeking loans to use their slaves as collateral and took possession of some of them when their owners defaulted. Like New York Life, Aetna and US Life also sold insurance policies to slave owners, particularly those whose laborers engaged in hazardous work in mines, lumber mills, turpentine factories and steamboats in the industrializing sectors of the South. US Life, a subsidiary of AIG, declined to comment on its slave policy sales. Wachovia, one of Wells Fargo’s predecessor companies, has apologized for its historic ties to slavery as have JPMorgan Chase and Aetna.

More than 40 other firms, mostly based in the South, sold such policies, too, though documentation is scarce and most closed their doors generations ago. New York Life survived. Its foray into the slave insurance business did not prove to be lucrative: The company ended up paying out nearly as much in death claims — about $232,000 in today’s dollars — as it received in annual payments. But in the span of about three years, it sold 508 policies, more than Aetna and US Life combined, according to available records. Now, the descendants of one of those slaves — who were recently identified by The New York Times — are coming to terms with the realization that one of the nation’s biggest insurance companies sold policies on their ancestors and hundreds of other enslaved laborers.

The company’s connections to slavery drew attention in the early 2000s as California and more than a dozen localities, among them Chicago, Philadelphia and San Francisco, began to require companies to disclose their slavery-era activities. The disclosure laws emerged in response to black activists and lawyers who pressed for reparations and a public reckoning with history. (A lawsuit filed against New York Life and other companies tied to slavery was dismissed in 2004 after a judge ruled that the African-American plaintiffs had established no clear link to the businesses they sued and that the statute of limitations had run out more than a century ago.”

VIRGINIA SLAVE BREEDERS

https://aaihs.org/the-capitalized-womb/

https://blog.oup.com/2012/01/slave-trade

https://wnyc.org/story/ned-and-constance-sublette

https://monticello.org/thomas-jeffersons-attitudes-toward-slavery

https://kottke.org/a-history-of-the-slave-breeding-industry-in-the-united-states

https://psmag.com/social-justice/a-future-history-of-the-united-states

The American Slave-Breeding Industry, researched by Ned & Constance Sublette

reviewed by Malcolm Harris / Jan 26, 2016

“The American Slave Coast is a big book, both physically (over 700 pages including citations) and conceptually. From the colonial period to the postbellum, the authors Ned and Constance Sublette cast slavery, and the slave-breeding industry, as the center of American history. It’s a provocative and nightmarish thesis, so distant from conventional ideas about America’s history that it feels like a dispatch from an entirely different time and place. If America had lost the Cold War, maybe this is how kids would be learning the nation’s story.

There’s an important fundamental difference between the history of slavery in the United States and a “history of the slave-breeding industry,” as The American Coast is subtitled. Slavery, in simplest terms, was unpaid labor. Slaves were shipped from Africa to the American South, where they cultivated tobacco and picked cotton and served owners but didn’t get paid and couldn’t leave. Slowly, reformers and abolitionists chipped away at the institution, first banning the Transatlantic trade, then fighting a civil war to eliminate human bondage. Freeing the slaves destroyed the South’s pseudo-feudal economy, ending the region’s economic dominance. That’s the story.

But to think about American slaves merely as coerced and unpaid laborers is to misunderstand the institution. Slaves weren’t just workers, the Sublettes remind the reader—they were human capital. The very idea that people could be property is so offensive that we tend retroactively to elide the designation, projecting onto history the less-noxious idea of the enslaved worker, rather than the slave as commodity. Mapping 20th-century labor models onto slavery spares us from reckoning with the full consequences of organized dehumanization, which lets us off too easy: To turn people into products means more than not paying them for their work.

One of the central misconceptions the Sublettes seek to debunk is the subordination of American slavery to the transatlantic trade. Conceptually locating the center of the slave trade offshore is good for America’s self-image, and it’s an old line. The Sublettes quote Southern slavers who blamed English firms for forcing the barbaric mode of transportation on America. In schools, the 1808 ban on capturing and shipping slaves is taught as part of the end of slavery, but the Sublettes re-frame it as simple protectionism: Domestic producers wanted to lock out foreign competition. In fact, most American slaves were not kidnapped on another continent.

Though over 12.7 million Africans were forced onto ships to the Western hemisphere, estimates only have 400,000-500,000 landing in present-day America. How then to account for the four million black slaves who were tilling fields in 1860? “The South,” the Sublettes write, “did not only produce tobacco, rice, sugar, and cotton as commodities for sale; it produced people.” Slavers called slave-breeding “natural increase,” but there was nothing natural about producing slaves; it took scientific management. Thomas Jefferson bragged to George Washington that the birth of black children was increasing Virginia’s capital stock by four percent annually.

Here is how the American slave-breeding industry worked, according to the Sublettes: Some states (most importantly Virginia) produced slaves as their main domestic crop. The price of slaves was anchored by industry in other states that consumed slaves in the production of rice and sugar, and constant territorial expansion. As long as the slave power continued to grow, breeders could literally bank on future demand and increasing prices. That made slaves not just a commodity, but the closest thing to money that white breeders had.

It’s hard to quantify just how valuable people were as commodities, but the Sublettes try to convey it: By a conservative estimate, in 1860 the total value of American slaves was $4 billion, far more than the gold and silver then circulating nationally ($228.3 million, “most of it in the North,” the authors add), total currency ($435.4 million), and even the value of the South’s total farmland ($1.92 billion). Slaves were, to slavers, worth more than everything else they could imagine combined.

At the same time, slave owners could not afford to rest. “Rebellions existed wherever there was slavery, in every era,” the Sublettes write, “because everywhere, always, the enslaved were at war with their condition.” Owners counted them as capital, but slaves were living laborers, too, with their own rosy myth: When the spell of indenture was lifted—an event they imagined often—their power would be gone, and they would be left running for their lives. Call it The Haiti Nightmare.

In 1775 and again in 1812 the British offered freedom to slaves who fought against their owners. Spanish and British threats to colonial and then national independence were understood as threats to slavery; black Spanish soldiers in Florida, decked out in full military regalia, were particularly unsubtle. Preserving slavery was a central motive in the American colonies’ fight for independence.

Americans first learn about slavery as children, before adults are willing to explain finance capital or rape. By high school, young adults are ready to hear about sexual violence as an element of slavery and about how owners valued their property, but there’s no level of developmental maturity that prepares someone to grasp systemized monstrosity on this scale. Forced labor we can understand—maybe it’s even a historical constant so far.

Mass murder too. But an entire economy built on imprisoning and raping children? One that enslaved near 40 percent of the population? Even for the secular, only religious words seem to carry enough weight: unholy, abomination, evil. The Civil War, as part of the American myth, cleanses the nation of this evil. The nation tore itself apart, but in the end slavery was gone, the country re-baptized in an ocean of fraternal blood.

https://youtu.be/K1XWq0_P_hI

It’s a compelling, almost Biblical narrative, with Abe Lincoln looming like an Old Testament patriarch. But, as the Sublettes make clear, the full renunciation of slavery never really happened. White Americans didn’t want a revolution; in the North, they wanted to suppress the secessionists and maintain national continuity, which meant continuity with the slave power. A reader need only recognize the surnames of slavery profiteers—like “Lehman,” as in “Brothers”—to see that we never truly broke this continuity.

https://www.youtube.com/watch?v=NcIBD7Aj7BM

The nation’s failure to break with the slaver class is best embodied in the figure of Nathan Bedford Forrest. An orphan by 17, Forrest built a fortune on inequity. As a wealthy planter, slave dealer, speculator, racist, and murderer, he was a classic “self-made” American of the mid-19th century. As a Confederate cavalry commander, Bedford ordered the massacre of hundreds of black Union soldiers at Fort Pillow.

But when the South surrendered, the war criminal Forrest received a presidential pardon. When Forrest’s fellow Tennessee volunteers formed a paramilitary organization dedicated to white terror, they turned to the former lieutenant general for leadership. The “Wizard of the Saddle,” as Forrest was called, became the first Grand Wizard of the Ku Klux Klan.

The book directly addresses personal beliefs and behavior of presidents and other founders, but not as mere disturbing factoids that reveal heroes as villains. The authors indict the American ruling class as a whole, and in so doing they recast the fathers as, first and foremost, members of their class. The Sublettes don’t draw a line between political and economic history; legislation and state policy emerges directly from slaver class interest. America has always been run by millionaires, and by the time of secession, two-thirds of them lived in the South, with human beings composing most of their wealth.

To see the founders as first and foremost slavers is to see them as evil, but not necessarily in an epic or dynastic sense: The slaver class was paranoid and mean, petty and small. Contrary to the myths of American meritocracy, the country elevated the worst while terrorizing, torturing, and murdering the best. George Washington is introduced as the hapless jailer of Ona Judge, a 22-year-old slave of his wife Martha who escaped and “managed to avoid falling prey to the attempts at re-capture that George Washington attempted against her until he died.” The country’s great narratives, from independence to manifest destiny, the authors suggest, are all better understood as maintenance work on history’s most sinister asset bubble.

From rapist Jefferson who gave away his own daughter as a wedding present, to Andrew Jackson driving slaves shackled at the neck for Spanish gold, to Ben Franklin personally selling slaves on consignment as a newspaper publisher, to James Polk overseeing his brutal plantation from the floor of Congress, to young Woodrow Wilson at his father’s side while the latter preached the Christian virtue of white supremacy, there’s no end to the vicious degradation of Africans as America’s very foundation.”

Historian and author Edward E. Baptist explains how slavery helped the US go from a “colonial economy to the second biggest industrial power in the world.” https://t.co/tByX6muUCi

— Vox (@voxdotcom) August 22, 2019

ASSET SECURITIZATION

https://wsj.com/slavery-disclosure-law-will-apply-to-thousands-of-companies

https://vox.com/slavery-economy-capitalism-violence-cotton-edward-baptist

https://chicago.suntimes.com/american-finance-grew-on-the-back-of-slaves

American finance grew on the back of slaves

by Edward E. Baptist & Louis Hyman / 03/06/2014

“Last weekend we watched the Oscars and, like most people, were pleased that “Twelve Years a Slave” won Best Picture. No previous film has so accurately captured the reality of enslaved people’s lives. Yet though Twelve Years shows us the labor of slavery, it omits the financial system — asset securitization — that made slavery possible. Most people can see how slave labor, like the cotton-picking in “Twelve Years A Slave,” was pure exploitation.

Few recognize that a financial system nearly as sophisticated as ours today helped Solomon Northup’s enslavers steal him, buy him, and market the cotton he made. The key patterns of that financial history continue to repeat themselves in our history. Again and again, African-American individuals and families have worked hard to produce wealth, but American finance, whether in the antebellum period or today, has snatched black wealth through bonds backed by asset securitization.

Recently, the assets behind these bonds were houses. In the antebellum period, the assets were slaves themselves. Every year or two, somebody discovers that a famous bank on Wall Street profited from slavery. This discovery is always treated as if the relationship between slavery and the American financial system were some kind of odd accident, disconnected from the present. But it was not an accident. The cotton and slave trades were the biggest businesses in antebellum America, and then as now, American finance developed its most innovative products to finance the biggest businesses.

In the 1830s, powerful Southern slaveowners wanted to import capital into their states so they could buy more slaves. They came up with a new, two-part idea: mortgaging slaves; and then turning the mortgages into bonds that could be marketed all over the world. First, American planters organized new banks, usually in new states like Mississippi and Louisiana. Drawing up lists of slaves for collateral, the planters then mortgaged them to the banks they had created, enabling themselves to buy additional slaves to expand cotton production. To provide capital for those loans, the banks sold bonds to investors from around the globe — London, New York, Amsterdam, Paris. The bond buyers, many of whom lived in countries where slavery was illegal, didn’t own individual slaves — just bonds backed by their value. Planters’ mortgage payments paid the interest and the principle on these bond payments. Enslaved human beings had been, in modern financial lingo, “securitized.”

As slave-backed mortgages became paper bonds, everybody profited — except, obviously, enslaved African Americans whose forced labor repaid owners’ mortgages. But investors owed a piece of slave-earned income. Older slave states such as Maryland and Virginia sold slaves to the new cotton states, at securitization-inflated prices, resulting in slave asset bubble.

Cotton factor firms like the now-defunct Lehman Brothers — founded in Alabama — became wildly successful. Lehman moved to Wall Street, and for all these firms, every transaction in slave-earned money flowing in and out of the U.S. earned Wall Street firms a fee. The infant American financial industry nourished itself on profits taken from financing slave traders, cotton brokers and underwriting slave-backed bonds.

More recently, history repeated itself — or more accurately, continued. The antebellum world eerily prefigured the recent financial crisis, in which Wall Street securitization once again stepped in to strip black families of their wealth. In the 1990s red-lining began to end and black homeownership rates began to rise, increasing the typical family’s wealth to $12,100 by 2005 — or one-twelfth that of white households.

In those years, African-American family incomes were also rising about as rapidly as white family incomes. And yet, African-American buyers, playing catch-up after centuries of exclusion from the benefits of credit, still typically had lower net worth and credit ratings. They paid higher interest rates and fees to join the housing bubble, and so securitizing their mortgages brought enormous profits to lenders and investors.

Then the crash of 2008 came. By 2010, median African-American household wealth had plunged by 60 percent — all those years of hard work lost in fees, interest, and falling prices. For whites, the decline was only 23 percent, and those losses were short-lived. Lenders resumed lending to white borrowers, restoring the value of their assets. But African-American borrowers have had a much harder time getting new loans, much less holding on to property bought at securitization-inflated prices. Median white household wealth is now back up to 22 times that of blacks — erasing African-Americans’ asset gains over the preceding 20 years.

Recent foreclosures represent another transfer of wealth from African-Americans to the investors of the world. For the past 200 years, the success of American finance has been built on the impoverishment of African-American families. We should remember the heroic struggles of African Americans to get political equality, but to forget their exclusion from our financial system, except as a source of exploitation, is to miss a basic truth of not only black history but financial history.”

PREVIOUSLY

STILL in BUSINESS

https://spectrevision.net/2012/02/03/still-in-business/

LEGACY STATUS

https://spectrevision.net/2016/09/02/legacy-status/

CORNERED MARKETS

https://spectrevision.net/2016/09/22/cornered-markets/

SLAVE OWNER COMPENSATION PACKAGES

https://spectrevision.net/2018/04/11/slave-owner-compensation-packages/

COUNTER-REVOLUTION of 1776

https://spectrevision.net/2014/07/04/counter-revolution-of-1776/

WHERE SLAVE PENS ONCE STOOD

https://spectrevision.net/2009/01/19/where-slave-pens-once-stood/