Houses stand vacant in the Castlemoyne development in North Dublin, Ireland. {AP Photo/Peter Morrison}

VACANT HOUSING GLUTTONY

http://www.housingworks.utah.gov/documents/TEN-YEARPLAN.pdf

http://www.independent.co.uk/voices/comment/housing-first-good-news-for-the-homeless-this-christmas-9020934.html

Housing First: In Utah, homelessness may be about to become history

by Joseph Charlton / December 2013

Utah is on track to end homelessness by 2015. And it’s all down to one ingenious premise put forward by ex-state Governer Jon Huntsman eight years ago. Ending homelessness, said the one-time Republican leader candidate, could be achieved by giving those on the street one simple thing: a house. Thus the Housing First plan was born and in 2005 the first batch of Chronically homeless Utahans (yes, Utahans) were given apartments and full-time caseworkers. Alongside care from their assigned social worker, it was hoped each participant would become self-sufficient. But the beauty of the plan was that if the participant’s attempt at financial independence failed, they were still able to keep their place to live.

The reasoning behind the scheme was, of course, based on projected state-saving rather than outright benevolence. Utahan number crunchers calculated the annual cost of hospital and jail time for the average homeless person was costing the state $16,670, (£10,200) a year while an apartment and social worker would cost just $11,000. The numbers as well as the social benefits have been making sense ever since. Utah saves around $5000 on each rough sleeper moved indoors, and eight years on the rate of state homelessness has dropped by a staggering 78 per cent. And thankfully the scheme doesn’t just work in Utah. In Denver, Colorado – where a similar version of the programme has been put into effect – it was found prison incarceration costs for the housed homeless plunged by 76 per cent, while in-patient nights at hospitals were curbed by 80 per cent.

Now even more parts of America, including badly effected Wyoming, are considering copying the plan. The north western state’s homeless population has more than doubled in the last three years and yet fiscal restraint means only 26 per of those living on the streets are provided with shelter. Now, however, officials in Casper, Wyoming are planning to launch a programme modelled on the one pioneered by Utah. Let’s hope the good sense reaches the UK fast. An annual “state of the nation” report found homelessness in Britain was up by 6 per cent this year in England, and 13 per cent in London. If the Americans can find a way of saving money while helping those in need, can’t we do the same?

“It costs about $40,000 a year for a homeless person to be on the streets,” HUD secretary Shaun Donovan on “The Daily Show”, March 2012

SOCIALISM CHEAPER

http://www.pslweb.org/liberationnews/newspaper/vol-7-no-2/socialism-guarantees-the-right-to-housing.html

http://www.politifact.com/truth-o-meter/statements/2012/mar/12/shaun-donovan/hud-secretary-says-homeless-person-costs-taxpayers/

HUD secretary says each homeless person costs taxpayers $40,000 a year

by Molly Moorhead / March 5, 2012

The U.S. Department of Housing and Urban Development upped its cool quotient when Secretary Shaun Donovan appeared on The Daily Show with Jon Stewart. Donovan and Stewart exchanged small talk about growing up in New York City before turning to the topic of homelessness. “The thing we finally figured out is that it’s actually, not only better for people, but cheaper to solve homelessness than it is to put a band-aid on it,” Donovan said in the March 5, 2012, appearance. “Because, at the end of the day, it costs, between shelters and emergency rooms and jails, it costs about $40,000 a year for a homeless person to be on the streets.” Stewart then mentioned the costs of mental health services for homeless, who suffer a high rate of mental illness. Here, we’re looking at whether Donovan presented an accurate dollar figure.

Housing First

By emphasizing the high cost of leaving homeless people on the street, Donovan is reflecting a movement among homeless advocates and governments toward a model called “housing first.” Pioneered in the 1990s in New York City, it puts street dwellers in publicly subsidized rooms of their own and connects them with drug treatment, job placement and psychiatric services with the goal of stabilizing their lives. Unlike many treatment programs, housing-first initiatives don’t require participants to get sober first. “Housing first is a kind of ‘come as you are’ approach. We encourage folks to accept services, and as a result people change their behaviors,” said Brenda Rosen, executive director of Common Ground, a housing-first homelessness program in New York City. The approach succeeds and saves money, advocates say, because it targets the chronically homeless — those who have been homeless for a year or more and commonly suffer from addiction or mental illness. That segment of the homeless population uses expensive public services at very high rates — emergency rooms, police and fire, and courts.

Lake City Custom Homes is asking $750,000 for six-bedroom, 5,000-square-foot home in Herriman. {Danny Chan La, Deseret Morning News}

Donovan’s office pointed to a study by University of Pennsylvania researcher Dennis Culhane titled “Public Service Reductions Associated with Placement of Homeless Persons with Severe Mental Illness in Supportive Housing.” Culhane analyzed the costs of 4,679 mentally ill homeless people in New York City who were placed in supportive housing that also provided social services. Those costs were compared to data on people who relied on public shelters, public and private hospitals and correctional facilities. Culhane found that “persons placed in supportive housing experience marked reductions in shelter use, hospitalizations, length of stay per hospitalization and time incarcerated. Before placement, homeless people with severe mental illness used about $40,451 per person per year in services (1999 dollars). Placement was associated with a reduction in services use of $16,281 per housing unit per year.” This study is a decade old (the dollar figures are 13 years old), and it examined a subgroup of homeless people — those with severe mental disabilities — who need more services and thus have a higher cost of care. Donovan’s statement didn’t make that distinction; he just said ‘a homeless person.’

Plenty of other studies have attempted to determine the cost of homelessness, although with different variables such as city, age, addiction history, employment history and childhood background. For example, the Economic Roundtable in Los Angeles looked at the costs of homelessness there and reached similar conclusions. The 2009 study “Where We Sleep: The Costs of Housing and Homelessness in Los Angeles,” which followed 10,193 homeless individuals, found that the typical public cost for services for residents in supportive housing was $605 a month. For the homeless the cost was $2,897. The rate of $2,897 per month totals about $35,000 a year. “This remarkable finding demonstrates that practical, tangible public benefits result from providing supportive housing for vulnerable homeless individuals,” the researchers wrote.

![]()

Houses with discontinued construction surround an empty lot in Miami

For guidance on this story, we talked to Philip Mangano, the former homelessness policy czar under President George W. Bush. Mangano helped expand housing-first programs — with federal dollars behind them — into cities around the country. As the programs became established, Mangano said he was able to compile data from 65 cities looking at all services affected by homelessness. Hospitals, police and courts top the list. Chronically homeless people are regular visitors to emergency rooms, and each visit results in a hefty bill. They also frequently use mental health and addiction treatment services. They tend to rack up lots of arrests, leading to costly jail stays and use of court time. “They randomly ricochet through very expensive services, Mangano said. Mangano even looked at the impact on libraries, finding that many of them had to hire extra security to handle homeless loiterers.

Using data from the 65 cities — of all different sizes and demographics — the cost of keeping people on the street added up to between $35,000 and $150,000 per person per year, Mangano said. Conversely, after the housing-first programs had been established, Mangano said, he looked at the cost of keeping formerly homeless people housed. That range: $13,000 to $25,000 per person per year. “We learned that you could either sustain people in homelessness for $35,000 to $150,000 a year, or you could literally end their homelessness for $13,000 to $25,000 a year,” he said.

Why does it work? Rosen said housing people eliminates risk factors related to sleeping on the street, such as exposure to harsh temperatures and unhealthy drug habits that go untreated. Supportive housing, by contrast, provides a healthy environment. “Not only do you have support services on site, we build beautiful buildings and beautiful apartments,” she said. “You bring somebody inside, and you help restore their dignity. The support services that we offer help folks decrease their reliance on drugs. If they have mental health issues, they see a psychiatrist. And oftentimes their behavior is changed.”

Donovan said it costs the public $40,000 for a homeless person to be on the streets because of the expenses of emergency room visits, jail time and hospital stays. He drew that figure from a 10-year-old study that wasn’t looking at the general homeless population but at people with severe mental illness — a group that uses more services. The study also focused on New York City, an expensive place to live. Though Stewart and Donovan had been talking about growing up in New York shortly before, it wasn’t clear that Donovan was referring only to New York when he noted the costs of homelessness. But based on what we learned about the housing-first approach to ending homelessness, Donovan’s underlying point, as well as the dollar figure he cited, hold up. Mangano told us it costs between $35,000 to $150,000 in public services for one year of someone living on the street. That puts Donovan’s figure at the low end of the range, and it’s an outdated figure that would surely be higher now.

SHADOW INVENTORY

http://www.charlotteobserver.com/2012/01/01/2889998/housing-glut-looms.html

http://portlandtribune.com/pt/9-news/154848-cities-use-creative-means-to-deal-with-vacant-building-glut

http://nation.time.com/2013/08/15/this-land-is-your-land-when-desperate-cities-give-away-homes/

http://www.salon.com/2008/04/28/unoccupied_homes/

Overbuilt America – 18.6 million housing units in the United States are unoccupied

by Andrew Leonard / April 28, 2008

As of the end of March, 2008, there were 129.4 million “housing units” in the United States. According to a report released by the Census Bureau on Monday, 18.6 million of those homes are unoccupied — an increase of one million over the first quarter of 2007. 18.6 million unoccupied homes sounds like an awful lot. But that number is a little misleading. 4.7 million are for “seasonal use” only, the Census tells us — unoccupied vacation homes, in other words. 4.1 million are for rent, 2.3 million are for sale, and the remaining 7.5 million “were vacant for a variety of other reasons.”

The key figure is 2.3 million — the total number of homes that are empty and for sale. That adds up to a vacancy rate of 2.9 percent, which is the highest, reports Bloomberg, “since the bureau started keeping count in 1956.” 2.2 million homes were vacant and for sale one year ago. According to the Department of Housing and Urban Development’s Second Annual Homeless Assessment Report to Congress, released in March 2008, “the total number of homeless persons reported on a single night in January 2006 was 759,101.” Assuming that number bears some reasonable relation to reality, that would mean there are 24 unoccupied homes for every homeless person in the United States.

Only a 45-minute drive from downtown Madrid, towering vacant apartment blocks loom over empty streets and weed-filled lots. Apartments galore are for sale and rent, and prices are plunging. {AP Photo/Paul White.}

ENOUGH EMPTY HOUSES for the ENTIRE POPULATION of BRITAIN

http://wagingnonviolence.org/feature/chicagos-quiet-home-liberation-front/

http://www.dnainfo.com/chicago/20130609/rogers-park/bus-tour-highlights-trauma-of-foreclosure-eviction

http://articles.chicagotribune.com/2012-03-13/business/ct-biz-0313-foreclosure-squat–20120313_1_vacant-home-community-group-duplex-home

http://nytimes.com/2013/06/02/magazine/how-chicagos-housing-crisis-ignited-a-new-form-of-activism.html

http://www.storyleak.com/recovery-us-enough-empty-houses-hold-population-of-britain/

by Daniel G. J. / August 6th, 2013

Here’s a sobering statistic to consider next time you see a media hype piece about the ‘real estate recovery’: There are still over 14 million homes sitting empty in the United States. At four people per household, it is enough to comfortably hold the population of Britain. The Census Bureau actually keeps track of the number of empty houses, and the numbers it found in the last report are bothersome. They indicate that the real estate market is still far from recovery despite the media claims of a new housing boom. It’s an improvement over 2009 when there were 18.7 million homes sitting empty, but it’s still a bothersome figure.

Despite the TV networks’ claims of real estate in recovery, there are still 90,566 vacant foreclosures in Florida alone. There are 28,821 vacant foreclosures and distressed homes in California, where the real estate market is supposed to be recovering. Ohio has 17,367 vacant houses, mostly foreclosures. These figures don’t include other vacant homes, such as empty rentals and houses that have simply been abandoned. The worst-hit city is Las Vegas, which still has 40,481 vacant single family homes, 5,137 empty townhomes, and 16,542 empty condominiums. These figures were found by the Lied Institute for Real Estate Studies at the University of Nevada at Las Vegas’s Lee Business school. The study has been posted online here. The city with the most empty homes, to nobody’s surprise, is Detroit, which reportedly has 79,000 vacant homes. Some of which have been sitting empty for decades. What this means is that despite claims about recovery, there is still a vast amount of real estate out there that is not selling. Some cities, including Las Vegas and Detroit, seem to be in absolute depression.

Some of the many empty newly built apartment buildings stand with their exterior window shutters closed in Sesena, Spain. {Jasper Juinen/Getty Images.}

The huge number of empty homes not only depresses the real estate market, but it hurts the whole community. In many areas, property taxes are the primary method of financing schools and local government. Empty houses don’t pay property taxes. Detroit, which has the most vacant homes, recently declared bankruptcy because it can no longer pay the pensions and salaries of its current and retired city workers. The truth is that the U.S. housing market is not in recovery. Instead, it appears to still be in depression, and the media doesn’t want to admit the fact.

Unsold houses lie next to land bought for development at the Castlemoyne housing estate on December 1, 2010 in Dublin, Ireland. {Peter Macdiarmid/Getty Images.}

GHOST ESTATES

http://news.bbc.co.uk/2/hi/europe/8653949.stm

http://www.npr.org/2013/05/13/176659544/an-entrepreneurial-seedling-sprouts-in-detroit

http://www.gizmodo.com.au/2014/01/ireland-is-tearing-down-thousands-of-empty-brand-new-ghost-homes/

Ireland Is Tearing Down Thousands Of Empty, Brand New ‘Ghost Homes’

by Kelsey Campbell-Dollaghan / 1 January 2014

Phoenix, Madrid: These are the cities we tend to hold up as examples of the havoc that construction booms — and busts — can wreak on a housing market. Ireland is in the news less, but its situation is just as dire; an estimated 300,000 brand-new Irish homes have sat empty for years. And now the government is demolishing them.

According to the BBC, one in five Irish homes is vacant. This glut of housing is a symptom of the truly gigantic building boom that hit Ireland in the early 2000s: Guest workers from all over Europe flocked to rural areas around the country, where speculative housing projects were popping up in droves. But just a few years later, as the global financial crisis took hold, it became clear that the demand just wasn’t there. In 2006, Irish economist David McWilliams named these developments “ghost estates,” and the name has stuck.

Today, people who did buy new homes are out hundreds of thousands of dollars, and more that 600 new developments across the country are abandoned. Many of these homes are poorly built — all but uninhabitable, even if the buyers were there — and some are dangerous: The New York Times reports that a two-year old wandered into one construction site this year and drowned. A similar situation developed in Spain, where thousands of units of new housing still sit vacant, attracting blight and crime. Spurred by stories like these, Irish officials are going to unprecedented lengths to fix their mistake, opting to demolish the brand-new homes. According to the NYT, the government plans to raze at least 40 developments by the end of 2014. Bulldozers will pull down hundreds of homes that once went to market for $US500,000 or more — symbolizing the grim reality that the illusive market for these luxury suburbs never existed, and never will exist.

BofA Donates, Demolishes Houses to Cut Foreclosures | Bloomberg

Are there other options? Possibly. One Detroit nonprofit recently started offering vacant homes to writers and artists in an effort to revitalize nearly empty neighborhoods, though the effects of such projects are untested. Another project, in Cleveland, turned an abandoned home into a solar greenhouse. Other cities are toying with ideas like turning empty units into homeless shelters, storage spaces, or shared workshops. But it’s not as simple as it sounds. When Ireland’s housing boom was in full swing, building codes were often treated more as suggestions (the New York Times uses the phrase “honour code”), which means that many of these structures aren’t even inhabitable. It’s hard to imagine a future for homes that rest on unstable foundations with plumbing systems that spew sewage regularly. Although they do serve as a tidy metaphor for the situation their country’s housing is in.

Blackstone’s Hidden Billionaires | Bloomberg

the ROAD to SERFDOM (cont.)

http://www.bloomberg.com/news/2013-08-29/wall-street-s-rental-bet-brings-quandary-housing-poor.html

http://www.zerohedge.com/contributed/2013-06-05/real-reason-housing-prices-have-skyrocketed

http://www.doctorhousingbubble.com/modern-day-feudalism-real-estate-landlords-wall-street-rental-buying-cash-buying/

The rise of modern day real estate feudalism: the new rentier class / 5 Dec, 2013

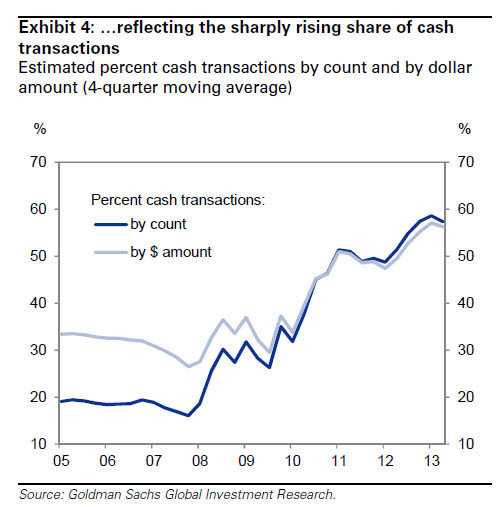

Feudalism was a set of customs in medieval Europe that setup a society in which relationships were based on holding land in exchange for service and labor. There is a modern day movement that is silently pushing out the middle class from truly owning real estate. In my view, there is no coincidence with the contracting US middle class and the massive expansion of “all cash” buyers. For most working Americans buying a home with all cash is so far removed from economic reality that it is not even an option. This used to be historically the case. However, since the Fed adjusted accounting rules and banks were able to control how inventory leaked out into the market, we suddenly have the highest number of cash and investors diving into the real estate market with alternative financing. People in Nevada, Arizona, and parts of Florida are competing with 50 to 60 percent of investors just to buy a home. In California the figure has been over 30 percent going back to 2009. Lower rates are a bigger pull for large investors since the safe trade in bonds or Treasuries is no longer there. So for this group, those 4 to 5 percent cap rate yields seem more attractive than the nearly non-existent rates on Treasuries. So we now have a system in place that is crushing the US homeownership rate and is shifting more property into concentrated hands.

Dan Barbiere searches through his household possessions after they were removed by an eviction team during a home foreclosure on October 5, 2011 in Miliken, Colorado. His wife Brandie said she had stopped making the mortgage payments 11 months before, after she lost more than half her home child care business due to the continued weak economy. A nationwide glut of foreclosed homes is expected to depress U.S. housing values for years. {John Moore, Getty Images}

First step, control that inventory

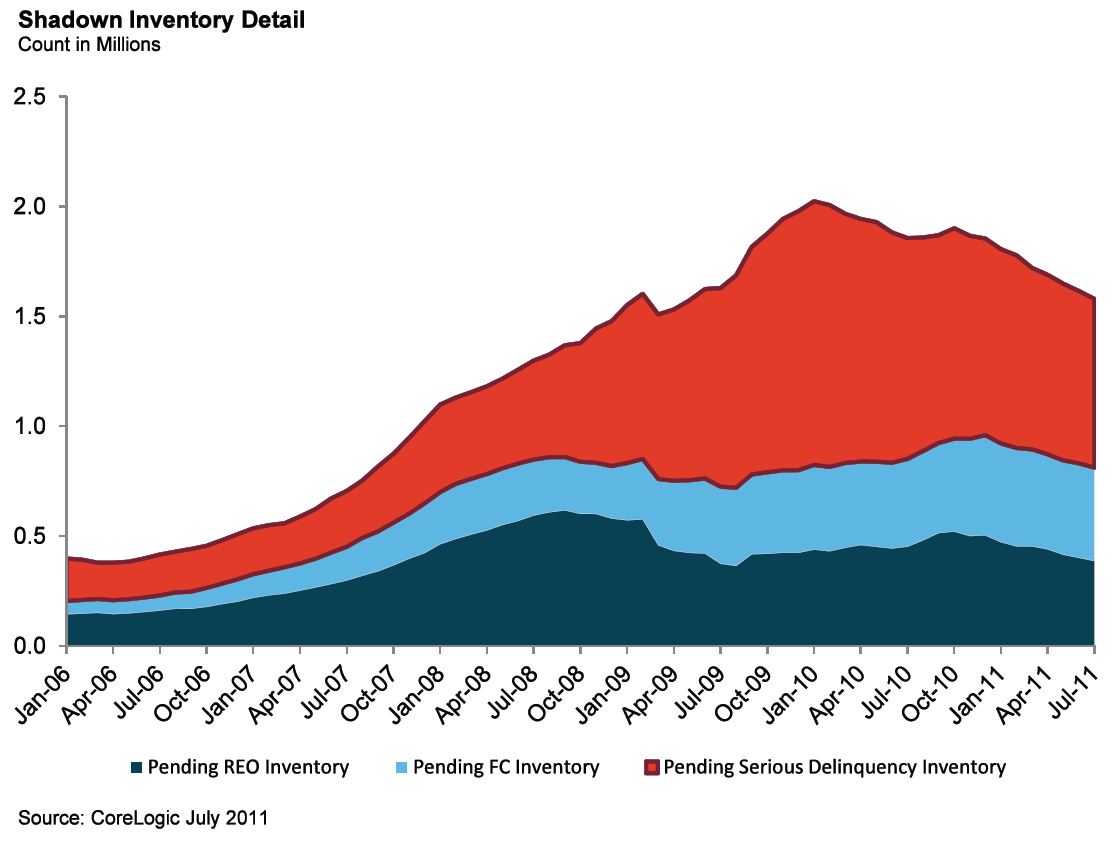

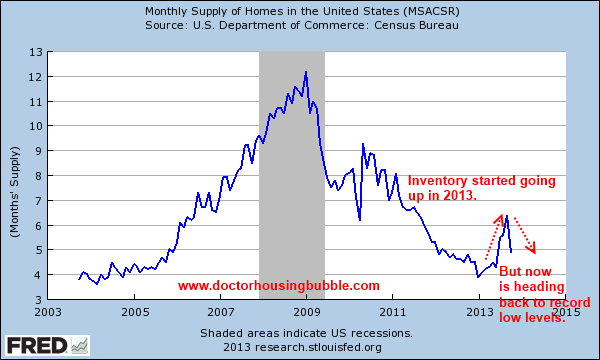

There was an interesting trend that started early this year. Nationwide inventory was starting to increase. Yet once rates spiked in the summer, that trend completely reversed:

Banks have an entire menu of methods of slowing down inventory that hits the market. Slowly since 2007, banks have figured out better methods of leaking out inventory. For example, freezing mark-to-market accounting and all the other programs that allowed for mortgage modifications. In some cases, the foreclosure process was dragged out 3 to 4 years! Yet the public face was to help average people but in reality, what has really occurred is a major shift from US household ownership of properties to investors swooping in and picking up properties on the cheap courtesy of modern day banking policy. In the end 5,000,000 Americans (and counting) still lost their homes via foreclosure and continue to do so. The massive spike in prices is allowing more people to exit mortgages they simply cannot afford by simply selling. Yet the drop in inventory is adding pressure to a market where sales are still weak. What you have is a fully controlled “market” where the Fed is buying up virtually all mortgages and investors instead of focusing on companies or more productive economic activity are becoming large scale landlords.

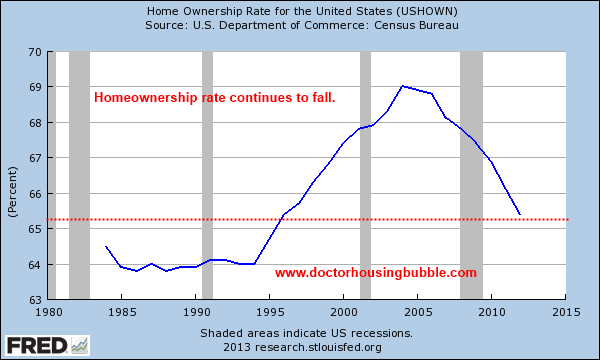

Prices up and homeownership down

Prices are up yet the homeownership rate in the US continues to fall:

How is this even feasible? For one, you might have one investor, purchasing a ton of properties:

“(Bloomberg) The market for rental-home securities may grow as large as $900 billion, assuming 15 percent of annual home purchases are conducted by investors and 35 percent of those and existing rental-home owners turn to the market for financing, according to Keefe Bruyette & Woods Inc. Banks have been the main source of financing for new property landlords such as Colony Capital LLC and Blackstone, which has spent $7.5 billion on about 40,000 houses.”

Instead of having 40,000 families buying those homes, you have a couple corporate owners. For nearly half a decade 30 percent of all US single home buying is going to investors. Historically, this figure was closer to 10 percent. That is a dramatic shift in the US real estate market. Did becoming a landlord suddenly become sexy for Wall Street?

With prices up dramatically in the last year including going up close to 30 percent in California, regular families are having a tougher time competing with the small amount of inventory available when investors are battling it out. What is interesting is also the number of rentals on the market has declined causing rents to spike. Household incomes are being eaten up either by higher home prices or higher rents as more households shift to renting adding pressure to the low supply of rentals. Ironically, we are not seeing a flood of these purchases hit the rental inventory market. Some are trying to flip which might explain the lack of rental inventory but this would add to overall sales inventory which has also fallen. This isn’t a full market so hard to guess what the next move is.

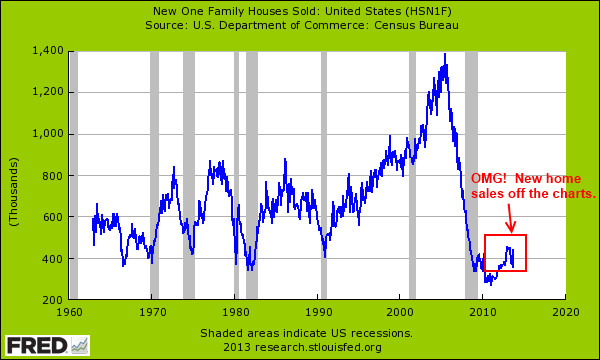

There was a big splash being made about the “massive” jump in new home sales. You want to see this big jump in context?

The chart above sums it up. All the action is happening in the existing home sale market and investors are dominating this game.

Cash buying

It is very clear that one-third of single family home purchases have gone to investors since 2009. However, some estimates put this figure a bit higher:

A safe number is one-third. In markets like Nevada, Arizona, and Florida it is closer to half. Even in Las Vegas, what regular working family is going to have $100,000 sitting around to make an all-cash offer? In California where a shack goes for $500,000 the game is even more bizarre. Yet people have to work and live somewhere. People for the most part are idle creatures. In California you have the conundrum of golden real estate handcuffs via Prop 13. People can sell and move to another state and have a healthy retirement but would rather eat cat food and live in a shack with low tax rates. It is an interesting trend especially with many baby boomers now seeing their kids coming back home with loads of college debt.

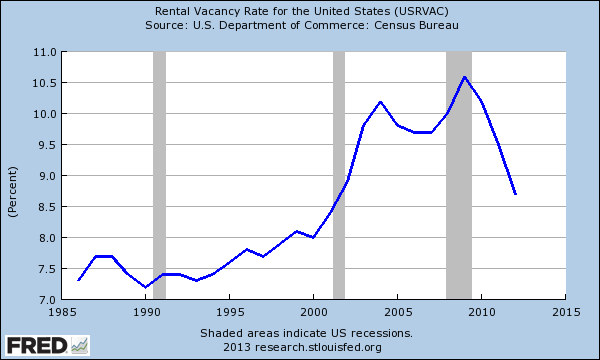

Rental market getting squeezed

The low supply and large investor buying is now causing a drop in the rental vacancy rate:

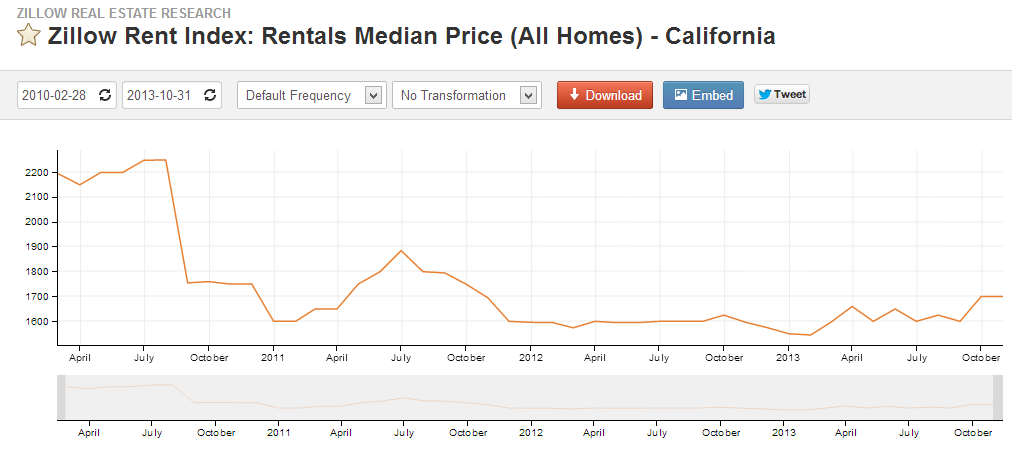

Because of this rents are moving up but in some markets are still below the record highs:

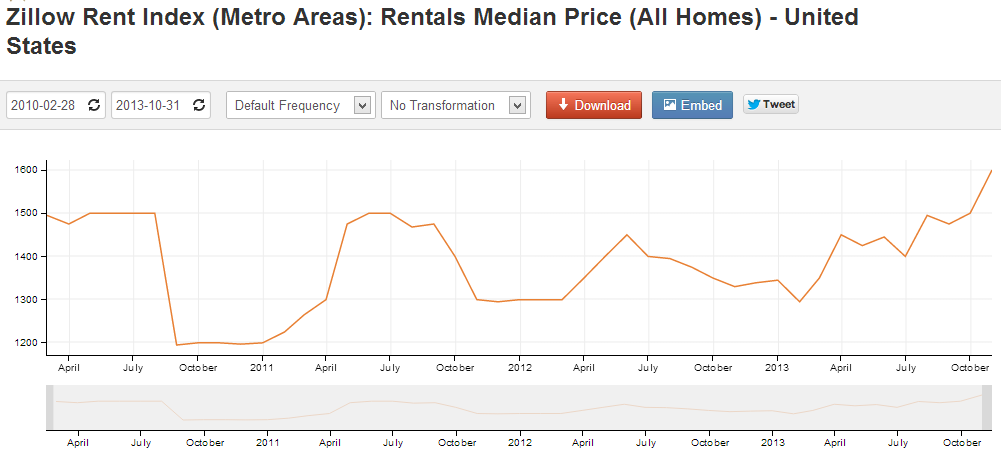

However nationwide rents are at an all-time record high:

Low inventory is a symptom of market manipulation. Too many odd incentives and banking shenanigans have created a distorted market. The Fed now owns 12 percent of the mortgage market and is essentially the only buyer of mortgage backed securities. Look at all the above data. Who do you think is really winning here? Rents are higher. Home prices are higher. Yet the menu of good employment opportunities is limited. Incomes are hardly increasing. The younger generation is massively in student debt and they are having a tough time finding good work. What an odd game of real estate we are living in.